Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

If you are responsible for processing payments in Bangladesh — whether as an accountant, finance manager, or business owner — you cannot afford to get the TDS and VDS rate wrong. A wrong rate means a wrong deduction. A wrong deduction means a penalty. And penalties from the NBR can be costly and time-consuming to resolve.

This guide gives you a clear, practical breakdown of the TDS and VDS rate in Bangladesh for FY 2025-26, based on the Income Tax Act 2023, the Withholding Tax Rules 2024 (SRO No. 161-Law/Income Tax-36/2024 dated 29 May 2024), and the Finance Ordinance 2025 effective from 1 July 2025.

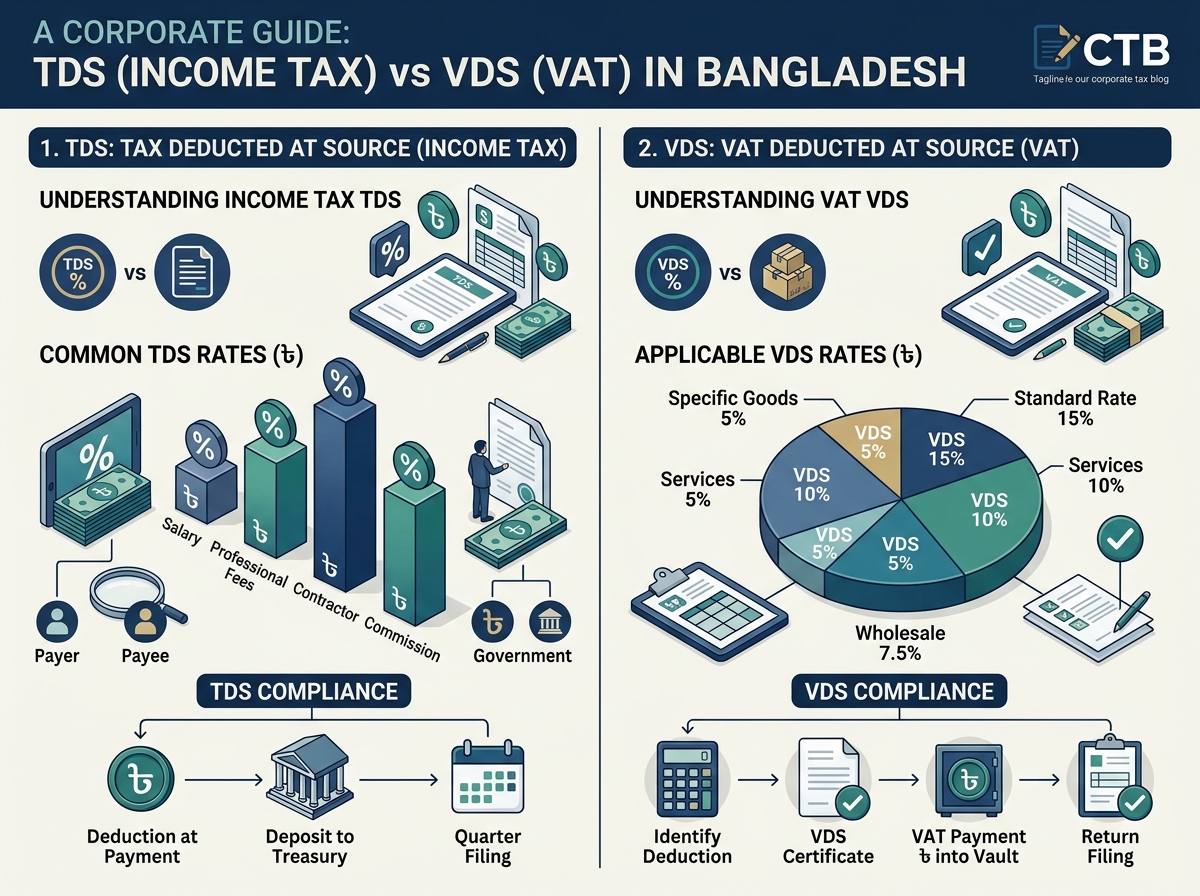

What Is TDS and Why Does It Matter?

TDS stands for Tax Deducted at Source. It is a system where the person making a payment deducts income tax at the applicable rate and deposits it directly to the government treasury — before the recipient gets the money.

Think of it this way: if your company pays Tk. 1,00,000 to a consultant, you do not pay the full amount. You deduct the applicable TDS, pay the consultant the net amount, and deposit the deducted tax with the NBR via treasury challan.

The entity deducting the tax is called the withholding entity, and this responsibility applies to businesses, NGOs, government bodies, and any organisation with an annual turnover above Tk. 1 crore.

VDS — VAT Deducted at Source — works on the same principle but applies to VAT on services rather than income tax. Both TDS and VDS must be deducted at the time of payment and deposited within the prescribed deadlines.

Getting the TDS and VDS rate in Bangladesh right is not just good practice — it is a legal obligation under the Income Tax Act 2023 and the VAT & SD Act 2012.

TDS Rate Chart for FY 2025-26 (Section-Wise Summary)

The following rates apply under the Income Tax Act 2023 as updated by the Finance Ordinance 2025. The key SRO governing these rates is SRO No. 161-Law/Income Tax-36/2024.

| SL | Payment Type | Section | Rate |

|---|---|---|---|

| 1 | Salary | 86 | Average Rate |

| 2 | Workers’ Profit Participation Fund (WPPF) | 88 | 10% |

| 3 | Supply of goods / services / contracts | 89 | See Annexure-1 (0.5%–10%) |

| 4 | Services (consultancy, IT, etc.) | 90 | See Annexure-2 (2%–15%) |

| 5 | Payment for intangible assets | 91 | 10% |

| 6 | Advertisement bill (newspaper/TV/radio) | 92 | 5% |

| 7 | Commission, discount and fee | 94 | 10% |

| 8 | Travel agent | 95 | 0.30% |

| 9 | Interest on savings & fixed deposits | 102 | Company/Trust: 20%; Others: 10% |

| 10 | Profit on sanchaypatra | 105 | 10% |

| 11 | House rent | 109 | 10% |

| 12 | Electricity purchase | 114 | 4% |

| 13 | Dividend | 117 | Company: 20%; Others (with TIN): 10%; (without TIN): 15% |

| 14 | Import | 120 | Up to 20% (Rule 8) |

| 15 | Export proceeds | 123 | 1% |

| 16 | Transfer of property | 125 | Min. 1.65% (land) / Tk. 1,000 per sq. metre (flat) |

| 17 | Non-resident income | 119 | See Annexure-4 (5.25%–30%) |

Tip: The rates above are simplified summaries. For detailed sub-categories (e.g., supply of rice vs. supply of industrial raw materials), always refer to the full Annexures under the respective rules.

Annexure-1 Highlights: Section 89 Rates (Supply of Goods & Contracts)

Section 89 is one of the most commonly used TDS provisions. Here are the key rates:

- General execution of contract: 5%

- Supply of essential food items (rice, wheat, potato, fish, onion, sugar, salt, edible oil, etc.): 0.5%

- Supply of MS Billets from locally procured scrap: 0.5%

- Supply of cotton and yarn: 1%

- Oil supplied by oil marketing companies: 0.6%

- Supply by sub-contractor of 100% export-oriented company: 1%

- Cement, iron, iron products, ferro-alloy (excluding MS Billets): 2%

- All kinds of fruits: 2%

- Supply of books (other than to government): 3%

- Industrial raw materials to a manufacturer: 3%

- Gas distribution company: 0.6%

- Supply of cigarettes, bidi, jorda, tobacco, gul: 10%

- Manufacturing, process, civil/construction/engineering work: 5%

- All other goods/cases: 5%

Annexure-2 Highlights: Section 90 Rates (Services)

Section 90 covers a wide range of services. Key rates are:

- Advisory or consultancy (individual): 15%

- Advisory or consultancy (company/firm): 7.5%

- Technical services / know-how / assistance: 10%

- Catering, cleaning, security, manpower supply, event management, courier, training: 10% on commission/fee or 2% on gross bill

- Print/electronic media (gross bill): 0.65%

- Mobile network operator: 12%

- Motor garage or workshop: 8%

- Transport / vehicle rental / carrying service: 5%

- Internet service: 5%

- Wheeling charge for electricity transmission: 3%

- Freight forwarding agent (gross bill): 1.5%

- Any other service not listed above: 10%

Important: Banks, insurance companies, financial institutions, and Mobile Financial Service (MFS) providers such as bKash, Nagad, and Rocket are exempted from TDS under Rule 4 of the TDS Rules 2024 in certain cases.

TDS on Non-Residents: Annexure-4 (Section 119)

If your company is making payments to a non-resident, different (and generally higher) rates apply. Key ones include:

- Advisory/consultancy (individual): 20%

- Professional services (individual): 20%

- Technical services / know-how: 20%

- Royalties / intangibles: 20%

- Interest: 20%

- Salary/remuneration: 30%

- Dividend (company/fund/trust): 20%; others: 30%

- Air/water transport (not covered by DTAA): 7.5%

- Supply of goods: 7.5%

- Capital gain: 15%

- Insurance premium: 10%

- Courier services: 15%

- Any other payment: 20%

Always check whether a Double Taxation Avoidance Agreement (DTAA) applies between Bangladesh and the non-resident’s country before applying these rates — DTAA rates may be lower.

VDS Rate Chart for FY 2025-26

VDS — VAT Deducted at Source — is governed by the VAT & SD Act 2012. Below are the most commonly encountered VDS rates for FY 2025-26:

| Service Description | Service Code | VDS Rate |

|---|---|---|

| AC Hotel | S001.10 | 15% |

| Non-AC Hotel | S001.10 | 10% |

| Restaurant | S001.20 | 5% |

| Decorators and Caterers | S002.00 | 15% |

| Motor Garage and Workshop | S003.10 | 10% |

| Construction Firm | S005.00 | 10% |

| Advertising Agency | S007.00 | 15% |

| Printing Press | S008.10 | 15% |

| Indenting Organisation | S014.00 | 15% |

| Freight Forwarders | S015.10 | 15% |

| Community Centre | S017.00 | 15% |

| Consultancy and Supervisory Firm | S032.00 | 15% |

| Audit and Accounting Firm | S034.00 | 15% |

| Security Service | S040.00 | 15% |

| House Rent / Office Rent | S074.00 | 15% |

| IT-Enabled Services | S099.10 | 5% |

| Transport (petroleum goods) | S048.00 | 5% |

| Transport (other than petroleum) | S048.00 | 15% |

| Land Development | S010.10 | 2% |

| Building Construction (up to 1,600 sq ft) | S010.20 | 2% |

| Building Construction (1,601 sq ft & above) | S010.20 | 4.5% |

| Event Management | S071.00 | 15% |

| Manpower Supply | S072.00 | 15% |

| Repair and Maintenance | S031.00 | 15% |

| Courier and Express Mail | S028.00 | 15% |

| Legal Advisor | S045.00 | 15% |

| Sponsorship Services | S099.30 | 15% |

| Credit Rating Agency | S099.50 | 15% |

| Product Sale on Online Marketplace | S099.60 | 15% |

How TDS and VDS Work Together: A Practical Example

Suppose your company receives a Tk. 2,00,000 bill from a security services firm.

TDS (Income Tax): Under Section 90 (Annexure-2), security services attract TDS at 2% on gross bill amount. So you deduct Tk. 4,000 as TDS.

VDS (VAT): Under service code S040.00, security services carry a VDS rate of 15%. VAT on the bill = Tk. 30,000. You deduct this and deposit it separately.

Net payment to the security firm = Tk. 2,00,000 − Tk. 4,000 (TDS) − Tk. 30,000 (VDS) = Tk. 1,66,000.

Both the TDS amount (Tk. 4,000) and the VDS amount (Tk. 30,000) must be deposited to the government via treasury challan within the prescribed deadline — typically by the 15th of the following month for VAT, and within 2 working days for TDS under the Income Tax Act 2023.

Common Mistakes to Avoid

- Applying a flat rate without checking the sub-category. Section 89 has over 15 different rates. Always check which sub-category your supply falls under.

- Forgetting non-resident withholding. Many companies pay foreign consultants without applying Section 119 rates. This is a non-compliance risk.

- Not checking DTAA applicability. If the non-resident is from India, UK, Singapore, or another treaty country, a lower DTAA rate may apply — but you need a tax residency certificate.

- Depositing TDS late. Under the Income Tax Act 2023, failure to deduct or deposit TDS on time attracts penalties and interest under Section 315.

- Confusing TDS rate with VDS rate. Both apply to the same transaction in many cases. They are separate obligations — one for income tax, one for VAT.

Key Takeaway

The TDS and VDS rate in Bangladesh for FY 2025-26 is governed by the Income Tax Act 2023, the TDS Rules 2024, and the VAT & SD Act 2012 — all updated under the Finance Ordinance 2025 effective 1 July 2025. Whether you are paying contractors, renting office space, or hiring consultants, knowing the correct rate is the first step to staying compliant.

When in doubt, always cross-check against the relevant section annexure and the latest NBR SROs. Tax law in Bangladesh changes regularly, and relying on last year’s rate chart is one of the most common — and avoidable — compliance errors I see in practice.

Download Link

Disclaimer: This blog is for general informational purposes only. It does not constitute professional tax advice. Always consult a qualified tax practitioner or refer to the official NBR publications for specific guidance.

Leave a Reply

You must be logged in to post a comment.