Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former Accounts Manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

Understanding the tax rate in Bangladesh is no longer optional — it is a legal obligation for every earning individual and every operating business. Whether you are a salaried employee in Dhaka, a freelancer working with overseas clients, a small business owner, or a multinational company, getting your numbers right from the start prevents costly penalties down the line.

This guide covers every major tax rate in Bangladesh for the assessment year 2025–26, including individual income tax slabs, corporate tax rates, minimum tax rules, surcharges, and the key changes introduced by the Finance Ordinance 2025. The data here is sourced directly from the National Board of Revenue (NBR) and the Finance Ordinance 2025, so you can trust every figure.

What Governs the Tax Rate in Bangladesh?

The tax rate in Bangladesh is set annually through the Finance Ordinance or Finance Act, which the government presents as part of its national budget. The current legislation sitting under it is the Income Tax Act 2023, which replaced the Income Tax Ordinance of 1984 — a law that had been in force for nearly four decades.

The Revenue Policy and Revenue Management Ordinance 2025 has since brought one of the most significant structural changes in recent memory: the formal dissolution of the National Board of Revenue (NBR) and the Internal Resources Division (IRD), replacing them with two new bodies — the Revenue Policy Division (RPD) and the Revenue Management Division (RMD). This separation of policy from administration is designed to improve accountability, transparency, and efficiency in Bangladesh’s tax collection system.

For taxpayers, the practical impact of the tax rate in Bangladesh is still administered through the same portals and compliance channels — but it is important to be aware of this structural shift as further procedural changes are expected.

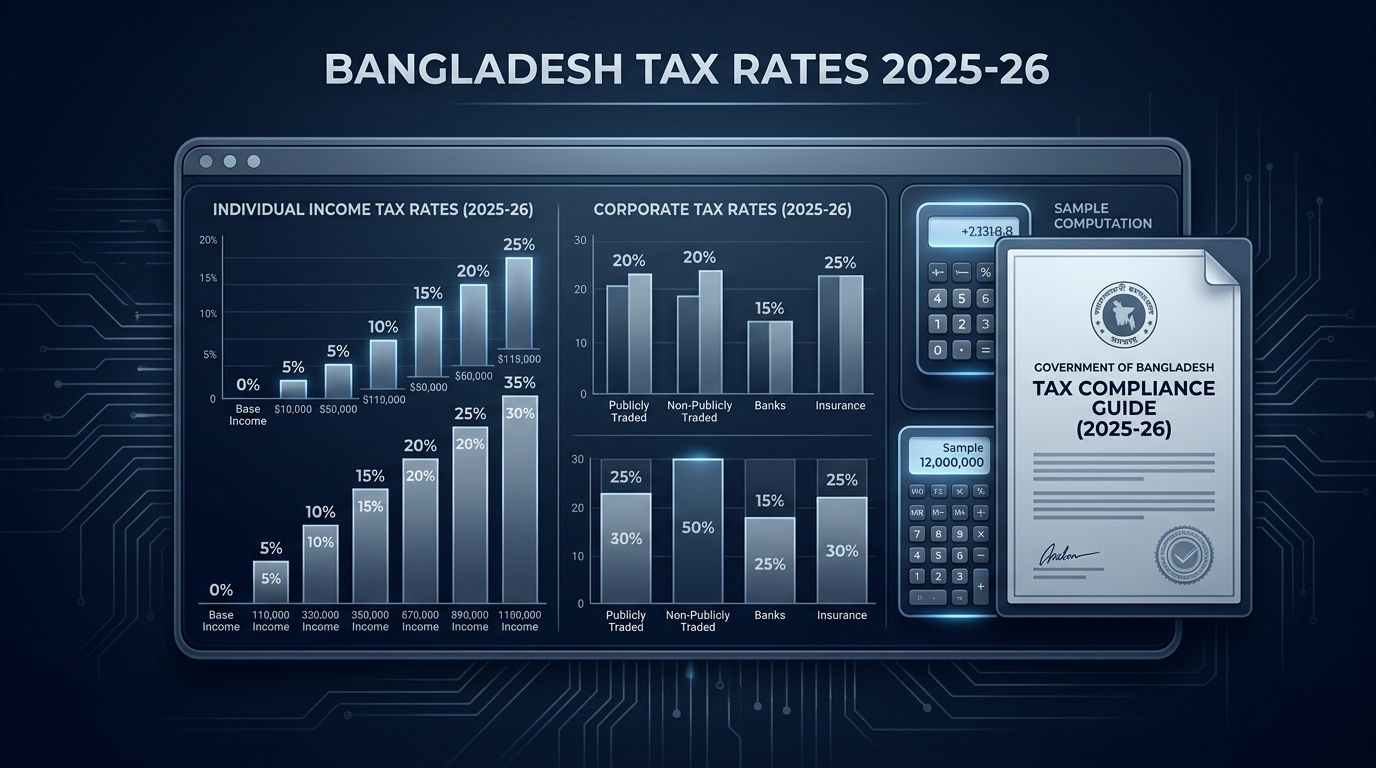

Individual Income Tax Rate in Bangladesh (AY 2025–26)

The bangladesh income tax rate for individuals follows a progressive slab system. This means the more you earn, the higher the rate applied to each additional tier of income. Here are the effective slabs for the assessment year 2025–26 (income year 2024–25):

| Taxable Income (BDT) | Tax Rate |

|---|---|

| Up to 350,000 | Nil (Tax-Free) |

| Next 100,000 | 5% |

| Next 300,000 | 10% |

| Next 400,000 | 15% |

| Next 500,000 | 20% |

| Next 2,000,000 | 25% |

| Above the above slabs | 30% |

The general tax-free threshold currently stands at BDT 350,000 per year. However, not everyone falls under the general category. Higher exemption limits apply to specific groups:

| Taxpayer Category | Tax-Free Limit (AY 2025–26) | Proposed Limit (AY 2026–27) |

|---|---|---|

| General taxpayers | BDT 350,000 | BDT 375,000 |

| Women & senior citizens (65+) | BDT 400,000 | BDT 425,000 |

| Persons with physical disabilities | BDT 475,000 | BDT 500,000 |

| Third-gender taxpayers | BDT 475,000 | BDT 500,000 |

| War-wounded gazetted freedom fighters | BDT 500,000 | BDT 525,000 |

Additional relief: Parents or legal guardians of a physically challenged child or adopted child receive an extra BDT 50,000 added to their tax-free threshold (one parent only, where both are taxpayers).

Practitioner’s note: The Finance Ordinance 2025 has proposed increases to the tax-free thresholds for the assessment years 2026–27 and 2027–28. These proposed changes are forward-looking and have not yet taken effect for your current filing. Do not confuse the proposed figures with the current operative rates.

Proposed Individual Tax Rate in Bangladesh for AY 2026–27 and AY 2027–28

The Finance Ordinance 2025 has locked in the following slab structure to apply from the next two assessment years:

| Taxable Income (BDT) | Tax Rate |

|---|---|

| Up to 375,000 | Nil |

| Next 100,000 | 5% |

| Next 400,000 | 10% |

| Next 500,000 | 15% |

| Next 500,000 | 20% |

| Next 2,000,000 | 25% |

| Above the above slabs | 30% |

The top marginal income tax rate of 30% remains unchanged. Non-resident individuals who are not Bangladeshi citizens also pay a flat rate of 30% on their total Bangladesh-sourced income.

Minimum Tax — A Critical Rule Every Taxpayer Must Know

Even if your calculated income tax falls below the threshold, you are still required to pay a minimum tax if your total income exceeds the tax-free limit. For the assessment year 2025–26, the minimum tax depends on your location:

| Location | Minimum Tax (AY 2025–26) |

|---|---|

| Dhaka North, Dhaka South & Chattogram City Corporations | BDT 5,000 |

| Other City Corporations | BDT 4,000 |

| Outside City Corporations | BDT 3,000 |

| New (first-time) taxpayers | BDT 1,000 |

From the assessment year 2026–27, a flat minimum tax of BDT 5,000 will apply to all taxpayers irrespective of location — simplifying the rule considerably. New taxpayers will continue to pay a reduced minimum of BDT 1,000.

Surcharge on High Net Worth Individuals

A surcharge applies on top of the regular tax rate in Bangladesh for individuals whose net assets exceed BDT 4 crore (BDT 40 million). The surcharge rates are applied progressively on the regular tax amount based on net wealth. Additionally, an environment surcharge applies to taxpayers who own more than one motor vehicle.

This is an area where many high-net-worth taxpayers make errors — particularly around declaring all assets correctly in their wealth statement. From my experience resolving audit disputes with the NBR, incomplete asset disclosure is one of the most common triggers for additional assessment.

Corporate Tax Rate in Bangladesh (AY 2025–26)

The corporate tax rate in bangladesh is not a single number — it varies significantly depending on the type of entity, its listing status, and the sector it operates in. Here is the full picture for the assessment year 2025–26:

| Entity Type | Tax Rate (Conditional) | Tax Rate (Unconditional) |

|---|---|---|

| Publicly listed companies | 20% | 22.5% |

| Non-listed companies | 27.5% | 30% |

| One Person Companies (OPC) | 22.5% | 25% |

| Banks & financial institutions (listed) | 40% | 42.5% |

| Banks & financial institutions (non-listed) | 42.5% | 45% |

| Mobile phone operators | 45% | 45% |

| Cigarette & tobacco manufacturers | 45% | 45% |

What Are the “Conditional” Lower Rates?

To qualify for the reduced corporate tax rate in Bangladesh, a company must satisfy strict banking channel requirements:

- All income and receipts must be transacted through bank transfer.

- All expenses and investments exceeding BDT 500,000 individually (or BDT 3.6 million in aggregate annually) must be made via bank transfer.

- Audited financial statements must be maintained and filed.

- Tax returns must be filed on time.

Failure to meet any of these conditions disqualifies the company from the reduced rate — and the difference is substantial. A non-listed company, for example, moves from 27.5% to 30% simply for routing a large payment through cash.

Minimum Tax for Companies

Companies are subject to a minimum tax on gross receipts — currently 0.25% on gross receipts — which is payable even in the case of a loss. The final tax liability is the highest of: (a) regular tax on profits, (b) applicable withholding tax (TDS) under relevant sections, or (c) the minimum tax on gross receipts.

This three-way comparison rule is a major compliance point. Many companies under-report their minimum tax liability by ignoring the gross receipts comparison — which the NBR auditors are trained to catch.

Investment Tax Rebate — Reduce Your Tax Legally

One of the most valuable and underutilised tools in Bangladesh’s tax system is the investment tax rebate. Resident and non-resident individual taxpayers can claim a tax rebate equal to 15% of their admissible qualifying investment.

The admissible investment is the lowest of:

- Actual eligible investment made

- 30% of total taxable income

- BDT 1 crore (BDT 10,000,000)

Qualifying investments include life insurance premiums, contributions to recognised provident or superannuation funds, purchases of savings certificates (Sanchayapatra), investments in approved securities, and contributions to approved pension funds. Even the purchase of a single laptop or PC qualifies.

From a practical standpoint, this rebate is the single most effective way to reduce your tax rate in Bangladesh impact — particularly for middle-income salaried professionals. Claim every eligible investment and keep receipts.

Salary Income Exemption (Important Update for AY 2025–26)

For salaried taxpayers, the Finance Ordinance 2025 has extended the salary income exemption ceiling. Previously, a salaried person could exclude one-third of total salary income or BDT 450,000 (whichever is lower) from taxable income. The Finance Ordinance 2025 raised the maximum ceiling to BDT 500,000.

This change directly reduces taxable income for many salaried employees, particularly mid-to-senior-level professionals — effectively lowering the individual tax rates they face in practice.

Non-Resident Bangladeshis (NRBs) and Non-Residents

The tax rate in Bangladesh applies differently depending on residency status:

- Resident individuals are taxed on worldwide income at progressive slab rates.

- Non-Resident Bangladeshis (NRBs) — Bangladeshi citizens living abroad for more than 182 days in a fiscal year — are taxed only on Bangladesh-sourced income (salary, rent, dividends, capital gains). Special NRB rates or double taxation treaty benefits may apply.

- Non-residents who are not Bangladeshi citizens are taxed at a flat rate of 30% on their total Bangladesh-sourced income. No slab benefit applies.

Bangladesh has double taxation agreements (DTTs) with a number of countries. If you live and work abroad, claiming treaty relief can prevent being taxed twice on the same income. Always obtain a Tax Residency Certificate from the relevant foreign authority before making a treaty claim.

Capital Gains Tax Rates in Bangladesh

Capital gains are treated separately from regular income under the income tax rates framework:

| Asset Type | Holding Period | Tax Rate |

|---|---|---|

| Securities (listed companies) | Any | Flat 10% |

| Other capital assets | ≤ 5 years | Added to total income at slab rate |

| Other capital assets | > 5 years | Flat 15% |

| Sponsor/Director shareholders (securities transfers) | Any | 10% (increased from 5%) |

For property transactions, gains are taxed based on location — with Dhaka, Chattogram, and Gazipur attracting higher per-square-metre rates compared to other areas.

Key Filing Deadlines and Penalties

Understanding the tax rate in bangladesh is only half the battle — compliance is the other half.

Filing deadlines for AY 2025–26:

- Individuals: March 31, 2026 (extended from the standard November 30 deadline)

- Corporations: Generally March 15; extended to April 15, 2026 for the current cycle

Penalties for non-compliance:

- Late filing: Immediate penalty of 10% of the tax on last assessed income (minimum BDT 1,000)

- Interest for failure to file on time: 2% per month on the outstanding tax computed under Section 174

- False declarations can attract legal proceedings

From 2025–26, proof of submission of return (PSR) is required in a growing number of everyday transactions — including applying for loans above BDT 5 lakh, registering a motor vehicle, obtaining a credit card, or enrolling children in English-medium schools with fees above BDT 1 lakh.

VAT — The Other Major Tax Rate in Bangladesh

While income tax is the focus of this guide, no overview of the tax rate in Bangladesh is complete without mentioning VAT. The standard Value Added Tax (VAT) rate in Bangladesh is 15%, levied on the transaction value of most imports and domestic supplies of goods and services. Bangladesh introduced VAT in 1991 under the VAT Act, with the current framework governed by the VAT and Supplementary Duty Act 2012.

Supplementary duties and customs duties add additional layers for specific goods — particularly imported items, tobacco, and luxury products.

Summary — Tax Rates in Bangladesh at a Glance (AY 2025–26)

| Tax Type | Rate |

|---|---|

| Individual income tax (lowest slab) | 5% |

| Individual income tax (highest slab) | 30% |

| Non-resident (non-Bangladeshi) flat rate | 30% |

| Corporate tax (listed companies, conditional) | 20% |

| Corporate tax (non-listed, conditional) | 27.5% |

| Banks & financial institutions (non-listed) | 42.5% |

| Mobile phone operators | 45% |

| Tobacco manufacturers | 45% |

| Standard VAT | 15% |

| Capital gains (listed securities) | 10% |

| Long-term capital gains (>5 years, other assets) | 15% |

| Investment tax rebate | 15% of eligible investment |

Final Word from the Author

Having spent over a decade navigating tax compliance across Bangladesh and the UK — and having personally represented clients through multi-year audit disputes with both the NBR and HMRC — I can tell you that the most expensive mistakes are never about the tax rate in bangladesh itself. They are about misunderstanding which rate applies, missing a deadline, or failing to claim a legitimate relief.

The Finance Ordinance 2025 has brought meaningful changes to exemption thresholds, minimum tax rules, salaried income exemptions, and the structural reform of tax administration. These changes create both opportunities and risks — and the window to plan around them is now.

If you are unsure about your own position — whether as an individual taxpayer, a small business, or a multinational operating in Bangladesh — take professional advice before filing. The cost of getting it right is always less than the cost of getting it wrong.

For the most current official rates, always refer to the NBR Bangladesh portal and the Finance Ordinance 2025 gazette notification.

© Md Rakib Hassan. This article is for informational purposes only and does not constitute legal or tax advice. Seek professional guidance for your specific situation.

Tags: tax rate in bangladesh, bangladesh income tax rate, income tax rates, corporate tax rate in bangladesh, individual tax rates, NBR Bangladesh, Finance Ordinance 2025, income tax slab 2025-26, minimum tax BangladeshShare

Leave a Reply

You must be logged in to post a comment.