Every VAT-registered business must maintain two foundational books. Mushak 6.1 and 6.2 books Bangladesh — the Purchase Account Book and Sales Account Book — feed the monthly Mushak 9.1 return and provide the primary audit trail for NBR.

Purpose of Mushak 6.1 and 6.2 Books Bangladesh

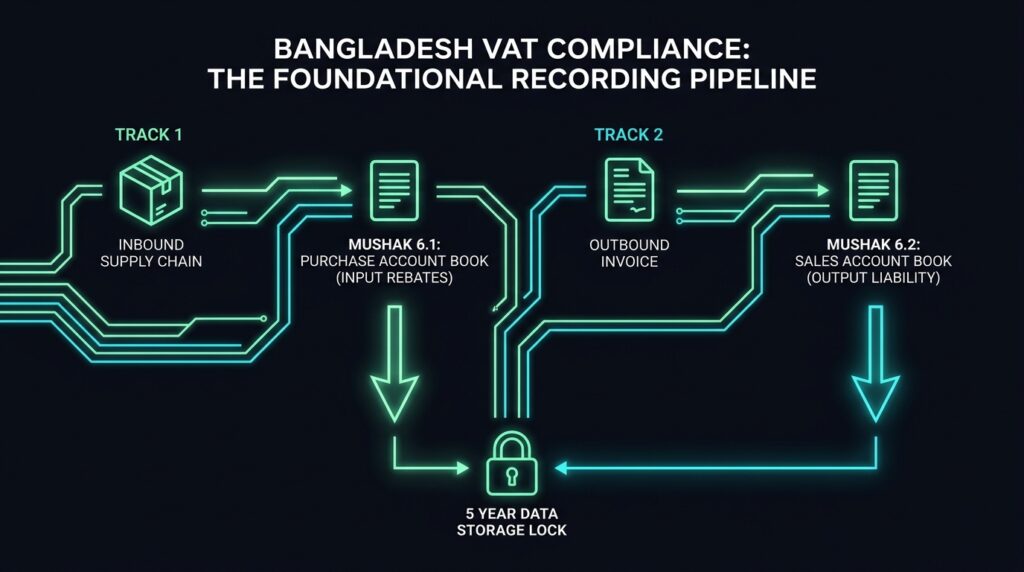

The Mushak 6.1 and 6.2 books Bangladesh are not optional; they’re prescribed under Rule 40 of the VAT & SD Rules 2016. Mushak 6.1 records every input purchase (with corresponding input VAT). Mushak 6.2 records every output supply (with corresponding output VAT).

Mandatory Fields in Mushak 6.1

The purchase book entries should capture:

- Date of purchase

- Supplier name and BIN

- Mushak 6.3 invoice number and date

- Description of goods/services

- Total invoice value

- Input VAT paid

- VDS (if any) deducted

- Reference to Mushak 6.6 received

Mandatory Fields in Mushak 6.2

The sales book entries should capture:

- Date of sale

- Buyer name and BIN (where applicable)

- Mushak 6.3 invoice number issued

- Description of goods/services

- Total invoice value

- Output VAT charged

- VDS (if any) suffered

- Reference to Mushak 6.6 received from buyer

Digital vs Physical Books

NBR permits Mushak 6.1 and 6.2 books Bangladesh in digital format through approved VAT software. Most businesses now maintain these electronically with automated population from invoicing systems. Physical book formats remain acceptable but are increasingly impractical for any active business.

Retention Period

Both books must be preserved for at least 5 years from the end of the relevant tax period. NBR auditors typically request access during VAT audits.

How Mushak 6.1 and 6.2 Books Bangladesh Feed Mushak 9.1

The monthly Mushak 9.1 return draws directly from these books:

- Input VAT total from Mushak 6.1 → claimable rebate

- Output VAT total from Mushak 6.2 → tax payable

- VDS suffered → decreasing adjustment

- VDS deducted → increasing adjustment

If your Mushak 6.1 and 6.2 books Bangladesh aren’t accurate, your Mushak 9.1 can’t be either.

Common Errors

In practice:

- Books not maintained current — month-end catch-up creates errors

- Missing supplier BIN in Mushak 6.1 entries

- Inconsistent voucher referencing between books and source documents

- No reconciliation against bank statements

Strategic Point

Mushak 6.1 and 6.2 books Bangladesh discipline is the foundation of everything else in VAT compliance. Build the daily-entry habit, and monthly Mushak 9.1 becomes routine.

Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

Need help with Mushak books, VAT, Income Tax, RJSC, or Accounting setup? We support businesses with end-to-end VAT bookkeeping across Bangladesh and the UK.

Leave a Reply

You must be logged in to post a comment.