Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm handling 1,000+ clients, with hands-on experience resolving multi-year audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

In nearly every audit I have closed over the last decade — whether in Dhaka or in London — the same pattern repeats. The substantive tax position is rarely the problem. The penalties and surcharges almost always trace back to a missed filing date, a delayed challan, or a return that was technically submitted but on the wrong form. A reliable, well-structured tax and VAT compliance calendar Bangladesh businesses can actually follow is, in my experience, worth more than any tax planning memo.

The FY 2025-26 cycle is particularly unforgiving. The Income Tax Act 2023 is now fully operational, the Finance Ordinance 2025 (issued on 2 June 2025) has rewritten several procedural rules, and on 12 May 2025 the government formally dissolved the National Board of Revenue (NBR) under the Revenue Policy and Revenue Management Ordinance 2025 — splitting tax authority between a new Revenue Policy Division (RPD) and a Revenue Management Division (RMD). For finance teams, this means the deadlines look familiar, but the authority you file with, the forms you use, and the penalty regime have all evolved.

This guide is the tax and VAT compliance calendar Bangladesh practitioners and CFOs need to keep next to the monthly close. It walks through every recurring obligation — monthly VAT and TDS, quarterly advance income tax, half-yearly and annual returns, regulatory filings with RJSC and Bangladesh Bank, and licence renewals — with the legal basis, the exact due date, the relevant form, and the penalty for slipping.

Why a Disciplined Compliance Calendar Matters in FY 2025-26

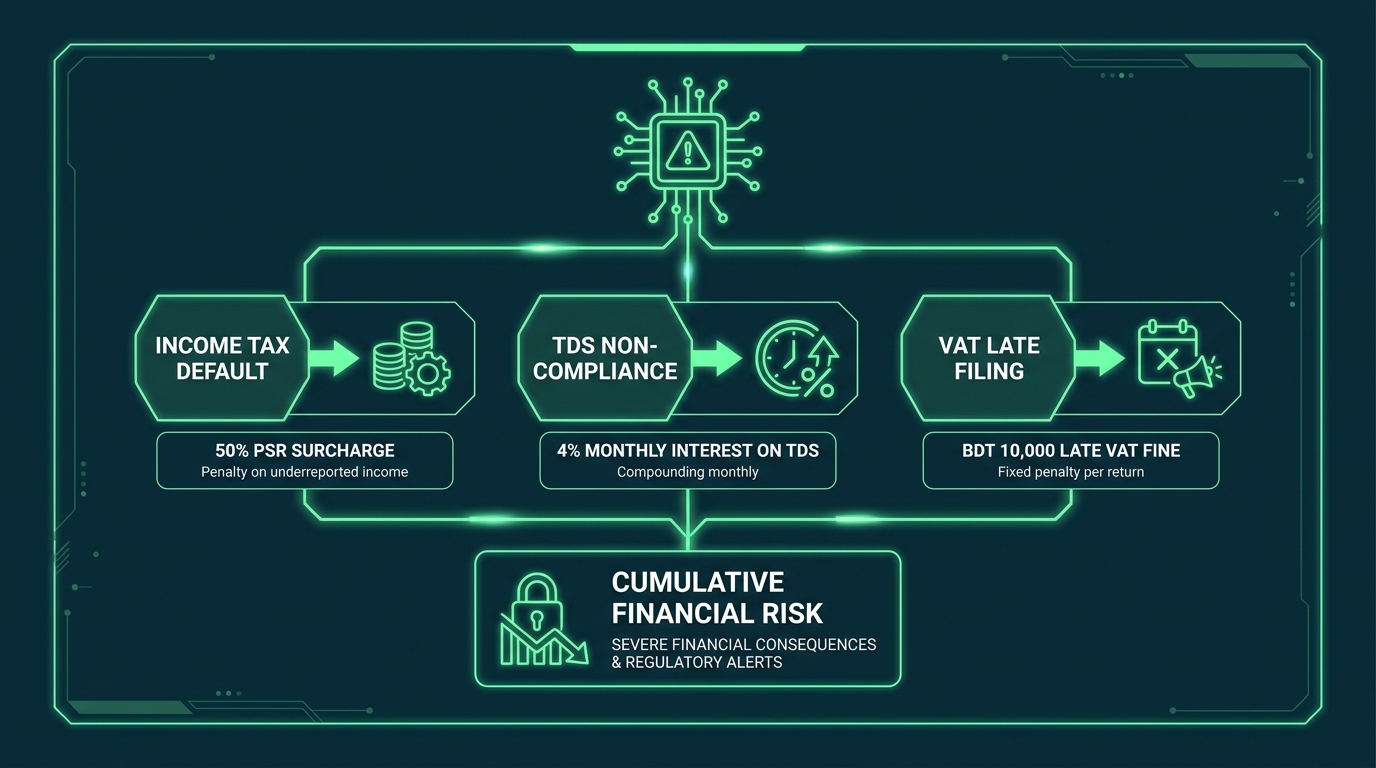

The cost of non-compliance in Bangladesh has quietly become more expensive than most management teams realise. Under the Income Tax Act 2023, the Deputy Commissioner of Taxes (DCT) now has a sharpened set of automated penalty triggers — interest at 4% per month on late tax payments, BDT 10,000 minimum for VAT return delays, and an additional 50% TDS surcharge on payments to persons without Proof of Submission of Return (PSR).

Three structural changes make the tax and VAT compliance calendar Bangladesh companies maintain in 2025-26 more critical than ever:

- Mandatory e-filing. From 4 August 2025, individual taxpayers must file income tax returns exclusively through the e-Tax portal (etaxnbr.gov.bd), with narrow exceptions for taxpayers aged 65+, persons with disabilities, and certain non-residents. The same digital-first push has hit VAT: a “Hard Copy Return Entry” sub-module was added to the iVAS portal in early 2026, requiring legacy paper returns to be digitised by 31 March 2026 to avoid automatic penalties.

- Tighter PSR enforcement. A Proof of Submission of Return is now needed for over 40 services, including trade licence renewals, bank loans above BDT 5 lakh, IRC/ERC renewals, and BIDA registration. Companies that maintain a clean compliance trail can transact freely; those who slip pay tax twice — first on the missed deadline, then on the doubled withholding when counterparties cannot find their PSR.

- The NBR split. Although most practitioners still informally say “NBR,” the legal architecture has changed. The VAT Commissionerate now operationally sits under the Revenue Management Division, while policy issues (rate changes, SROs, tax treaties) are handled by the Revenue Policy Division. For the bulk of FY 2025-26, filing portals, BIN, and TIN systems continue under the legacy infrastructure, but expect notifications and gazette references to start citing RPD and RMD.

Once you internalise these shifts, the rest of the tax and VAT compliance calendar Bangladesh becomes a discipline, not a guessing game.

Monthly Compliance Obligations

The monthly cycle is where most penalties are quietly accumulated. In my time managing accounts for a UK firm with Bangladesh-facing clients, I saw companies post a clean P&L every quarter — only to discover at year-end that monthly VAT returns had been filed late for six months running, triggering a cumulative penalty larger than their corporate tax bill.

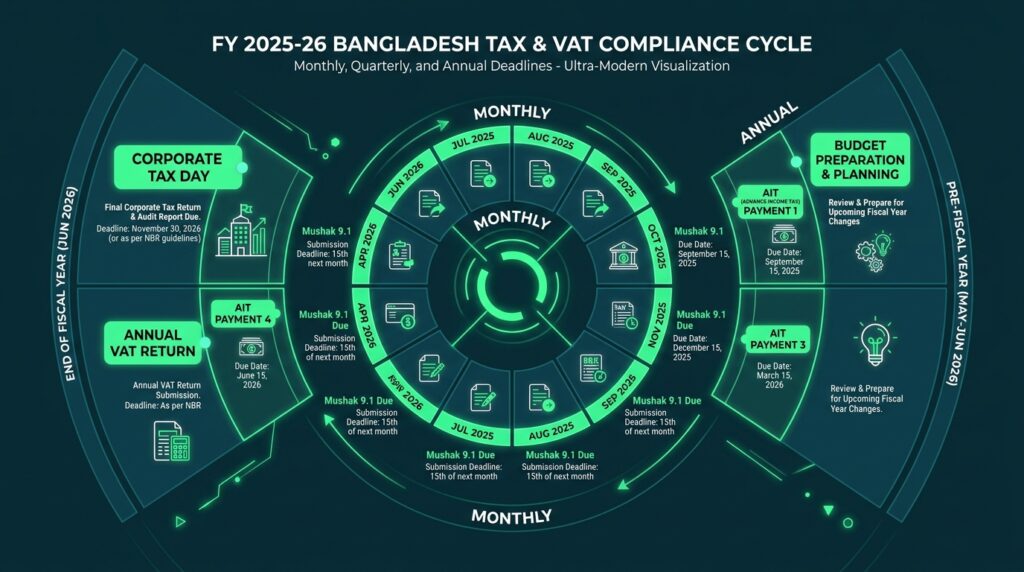

1. Monthly VAT Return — Mushak 9.1

- Form: Mushak 9.1 (Mushak 9.2 for turnover-tax enlisted persons)

- Deadline: Within the 15th day of the month following the tax period

- Legal basis: Section 64, VAT and Supplementary Duty Act 2012

- Authority: Local VAT Circle Office / submission via vat.gov.bd

- Payment of net VAT payable: Same date — by the 15th

- Penalty for late filing: BDT 10,000 plus simple interest at 1% per month on payable amount

Two practical traps. First, nil returns are mandatory — if your BIN-holding company had zero turnover in a month, you still must submit a nil Mushak 9.1. Second, the input tax credit (ITC) claim can only be made against a valid Mushak 6.3 invoice; informal purchase records will not survive a VAT audit, and disallowed ITC is one of the top three audit adjustments I see at NBR field offices.

2. VAT Deducted at Source (VDS) Deposit

- Deadline: By the 7th day of the next tax period for the VDS challan

- Legal basis: SRO No. 182-Ain/2025/268-Mushak dated 27 May 2025 (the consolidated VDS SRO for FY 2025-26)

- Authority: Designated bank → respective VAT Commissionerate

- Documentation: VDS challan reference must be quoted in your Mushak 9.1 of the corresponding period

3. Monthly Withholding Tax (TDS) Deposit

- Deadline: Within two weeks of the date of deduction (Section 142, Income Tax Act 2023)

- Form: Treasury Challan, deposited via Sonali Bank or authorised dealer banks

- Common TDS exposure: Salary (Section 86), payments to contractors and suppliers (Section 89), rent (Section 109), professional services (Section 90), interest on bank deposits, and dividend distributions.

4. Monthly Withholding Tax Statement to the DCT

- Deadline: By the 25th day of the following month (extended from the 15th by the Finance Act 2024 amendment, retained in FY 2025-26)

- Legal basis: Income Tax Act 2023, supporting Section 177 framework

- Authority: Deputy Commissioner of Taxes (DCT) of the relevant circle

- Content: Section-wise TDS deducted, challan numbers, deductee TIN and PSR status

A practical insight from audits I have personally negotiated: the DCT cross-references this monthly statement with the supplier’s own return. Mismatches — even small ones from a contractor’s misquoted TIN — frequently trigger spot-audit notices. Reconciling monthly is dramatically cheaper than defending the position eighteen months later.

Quarterly Compliance Obligations

The quarterly block of the tax and VAT compliance calendar Bangladesh is dominated by advance income tax and the consolidated withholding tax return.

5. Advance Income Tax (AIT) Instalments — Section 154

Companies and individuals whose last assessed income exceeded BDT 6,00,000 must pay advance tax in four equal instalments based on estimated annual tax liability:

| Instalment | Due Date | % of Estimated Annual Tax |

|---|---|---|

| Q1 | 15 September 2025 | 25% |

| Q2 | 15 December 2025 | 25% |

| Q3 | 15 March 2026 | 25% |

| Q4 | 15 June 2026 | 25% |

Under the Income Tax Act 2023, shortfalls between AIT paid and final liability attract simple interest at 4% per month on the under-paid amount, calculated from the original instalment due date — a meaningful cost on any material deferral.

6. Quarterly Withholding Tax Return — Section 177

The Income Tax Act 2023 introduced a quarterly filing requirement under Section 177, with the prescribed format provided through the Income Tax Rules. The obligation applies to:

- Government ministries, divisions, departments and directorates

- All companies (except MPO-listed educational institutions)

- NGOs and not-for-profits with statutory deduction obligations

- Banks, NBFIs and insurance companies

Filing dates (subject to the most recent SRO calendar):

- Quarter ending 30 September — file by 31 October

- Quarter ending 31 December — file by 31 January

- Quarter ending 31 March — file by 30 April

- Quarter ending 30 June — file by 31 July

Every TDS challan, deductee TIN, PSR reference, and section-wise breakup goes into this return. Missing or filing late triggers a penalty of 10% of the tax not deducted or collected, plus interest.

7. Quarterly FDI Reporting — Bangladesh Bank

Foreign-invested companies operating in Bangladesh must submit quarterly FDI inflow and stock returns to the Statistics Department of Bangladesh Bank via their authorised dealer (AD) bank:

- Deadline: Within 20 days of the end of each calendar quarter

- Form: ED Form (Statistical Returns on Foreign Investment)

- Authority: Bangladesh Bank, via AD bank

This is not strictly a tax filing, but it sits inside the same tax and VAT compliance calendar Bangladesh finance teams should maintain, because non-compliance jeopardises repatriation approvals — and I have seen profitable subsidiaries unable to remit declared dividends because their FDI reporting was three quarters behind.

Annual Compliance Obligations

8. Corporate Income Tax Return — Section 166 (Tax Day)

Under Section 2(73) of the Income Tax Act 2023, the Tax Day for a company is the 15th day of the seventh month following the close of its income year, or 15 September of the following financial year — whichever is later.

| Income Year End | Tax Day (Corporate Return Deadline) |

|---|---|

| 30 June 2025 (standard local companies) | 15 January 2026 |

| 31 December 2025 (banks, insurers, NBFIs) | 15 September 2026 |

| Other approved year-ends | 15th day of 7th month after year-end, or 15 September, whichever is later |

For AY 2025-26, the NBR (now operating as RMD) extended the company filing deadline to 17 May 2026 (15 May 2026 being a Friday). Where Tax Day falls on a government holiday, the next working day applies.

Mandatory attachments:

- Audited financial statements signed off by an ICAB-registered Chartered Accountant

- Document Verification System (DVS) reference number — without a valid DVS code, your audited accounts will be rejected at filing

- Tax computation sheet showing reconciliation from accounting profit to taxable income

- Statement of International Transactions (Section 238) where applicable

- Transfer Pricing return (Section 235) for taxpayers with cross-border related-party dealings exceeding the prescribed threshold

9. Individual Income Tax Return — Section 166

- Standard deadline for AY 2025-26: 30 November 2025

- Extended deadline (as notified by NBR): First extended to 31 December 2025, then to 31 January 2026 under Section 334 of the Income Tax Act 2023

- Mandatory e-filing: Through etaxnbr.gov.bd from 4 August 2025

Five categories are exempt from mandatory e-filing — taxpayers aged 65+, persons with certified disabilities, Bangladeshi residents living abroad, legal representatives of deceased taxpayers, and foreign nationals working in Bangladesh — though they may opt to e-file voluntarily.

10. Transfer Pricing Return — Section 235

Companies with international transactions with associated enterprises must submit a Transfer Pricing return alongside the corporate tax return. The form requires:

- Disclosure of all international transactions with non-resident related parties

- Selected transfer pricing method (CUP, RPM, CPM, TNMM, or PSM)

- Arm’s length analysis and benchmarking

- Auditor’s report in the prescribed TP format where transactions exceed BDT 3 crore in aggregate

11. International Transaction Return — Section 238

A consolidated information return is required for all international transactions with non-residents, filed with the annual corporate tax return. Penalties for non-filing can reach 1% of the value of transactions, capped at BDT 5 lakh.

12. RJSC Annual Return — Schedule X

- Deadline: Within 30 days of the Annual General Meeting (AGM)

- AGM itself: Must be held within 18 months of incorporation for the first AGM; within 15 months of the preceding AGM thereafter (or by the end of the next financial year, whichever is earlier)

- Authority: Registrar of Joint Stock Companies and Firms (RJSC)

- Penalty: Daily fine up to BDT 200+ for delay, plus risk of company being struck off the register

13. Licence and Permit Renewals

Many companies underestimate this section of the tax and VAT compliance calendar Bangladesh until they need a new bank facility or face an import-clearance hold-up.

| Licence / Certification | Renewal Deadline | Issuing Authority |

|---|---|---|

| Trade Licence | By 30 June 2026 (annually) | City Corporation / Pourashava / Union Parishad |

| IRC (Import Registration Certificate) | By 30 June 2026 | Office of the Chief Controller of Imports and Exports (CCI&E) |

| ERC (Export Registration Certificate) | By 30 June 2026 | CCI&E |

| Association Memberships (BGMEA, BKMEA, MCCI, etc.) | By financial year-end | Respective trade body |

| Fire Licence | Annual (date as per certificate) | Fire Service and Civil Defence |

| Environmental Clearance | As per ECC validity | Department of Environment |

| BIDA Registration | As per certificate validity | Bangladesh Investment Development Authority |

| BEPZA / BEZA permits | Per zone authority schedule | BEPZA / BEZA |

What Has Actually Changed in FY 2025-26 — The Practitioner’s View

Three changes deserve particular attention beyond the headline reforms.

First, presumptive tax has been raised. The Finance Ordinance 2025 increased the presumptive tax on gross receipts (for taxpayers who do not fall into a specifically categorised bracket) from 0.6% to 1%. For low-margin trading and service businesses, this is a real cost to model.

Second, funds no longer file returns. The Finance Ordinance 2025 confirmed that funds are not required to file income tax returns, with tax deducted on their income treated as final tax. Asset managers and trustees should update their compliance schedules accordingly.

Third, the “income difference” tax is gone. Section 20 of the Income Tax Act 2023, which charged tax on differences between import, export, or investment, has been repealed by the Finance Ordinance 2025. Multinationals with historically high cross-border flows should review prior-year provisions.

Fourth, the “out-of-country” filing rule has changed. Individuals who stayed abroad for higher education, deputation, lien employment, or on valid visa and work permit may now file within 90 days of returning to Bangladesh. This is genuinely helpful for expatriate professionals — but you must keep evidence of foreign stay and return.

Penalty and Surcharge Regime — What Actually Hurts

A working tax and VAT compliance calendar Bangladesh is not just about dates; it is about consequences. Here are the headline exposures under the current regime:

| Default | Penalty / Consequence |

|---|---|

| Late filing of Mushak 9.1 | BDT 10,000 plus 1% per month interest on payable VAT |

| Late deposit of TDS | 4% simple interest per month + disallowance of underlying expense |

| Late deposit of VDS | 2% interest per month plus penalty up to 50% of unpaid VAT |

| Late corporate tax return | Higher of: 10% of last assessed tax, or BDT 1,000 daily, capped at 50% of total tax payable (BDT 5,000 minimum) |

| Failure to file under Section 177 (TDS return) | 10% of tax not deducted/collected, plus interest |

| Non-compliance with DVS for audited accounts | Return is treated as defective; risk of best-judgement assessment under Section 183 |

| Missing PSR requirement | 50% additional TDS / TCS on payments made to the non-compliant party |

| RJSC Schedule X delay | Daily fine up to BDT 200+, plus risk of being struck off |

| FDI reporting default to Bangladesh Bank | Block on dividend repatriation and remittance approvals |

In one case I personally handled at the NBR Large Taxpayers Unit, a manufacturing client with otherwise clean books faced an additional liability close to BDT 1.4 crore — almost entirely composed of late-filing surcharges and disallowed TDS expenses, all of which would have been avoided with a structured calendar and a monthly close discipline.

How to Operationalise the Tax and VAT Compliance Calendar Bangladesh in Your Finance Function

Knowing the dates is the easy part. From running compliance for 1,000+ clients in the UK and supervising in-house teams for Bangladesh subsidiaries, these are the practices that actually keep the calendar working:

1. Build a single owner per filing. Every line on the tax and VAT compliance calendar Bangladesh should have one named owner. Shared responsibility is the single biggest reason filings slip.

2. Use a T-7 reminder model. Set internal deadlines seven calendar days ahead of the legal deadline. This gives you a week to fix challan mismatches, missing TIN data, or DVS sign-offs.

3. Reconcile TDS monthly, not annually. Match your General Ledger TDS expense, your treasury challans deposited, your monthly DCT statement, and your supplier ledger every month. Any variance discovered after 60 days becomes harder to resolve.

4. Maintain a digital evidence vault. Keep PDF copies of every Mushak 9.1 submission acknowledgment, every TDS challan, every Section 177 return, and every DCT correspondence — organised by financial year. NBR audit cycles routinely look back four to six years.

5. Build the tax and VAT compliance calendar Bangladesh into your statutory audit timeline. Your external auditor will need to verify all of this. Doing it in March, not in September, dramatically reduces audit fees and dispute risk.

6. Track licence expiries the same way you track tax. A lapsed Trade Licence will silently invalidate your VAT registration, which will silently disqualify your ITC claims, which will eventually surface as a VAT audit adjustment. The chain is real and I have unwound it more than once.

Frequently Asked Questions

Q1. Has the NBR really been abolished? Who do I file with now? Legally, yes — the National Board of Revenue was dissolved on 12 May 2025 under the Revenue Policy and Revenue Management Ordinance 2025, and replaced by the Revenue Policy Division (RPD) and the Revenue Management Division (RMD) under the Ministry of Finance. Operationally, however, the existing filing portals (etaxnbr.gov.bd and vat.gov.bd), BIN, TIN, and circle offices continue under the RMD. For FY 2025-26 you continue to file the same returns, with the same forms, to the same offices.

Q2. When is the corporate Tax Day for a company with a 30 June 2025 year-end? 15 January 2026 is the statutory Tax Day. For AY 2025-26, the NBR extended the deadline to 17 May 2026.

Q3. Is the Mushak 9.1 mandatory if I had no sales in the month? Yes. A nil return must still be submitted by the 15th of the following month. This is one of the most commonly missed compliances on the tax and VAT compliance calendar Bangladesh — and one of the easiest BDT 10,000 fines to avoid.

Q4. What is the AIT threshold for FY 2025-26? You must pay advance tax only if your total income in the last assessed year exceeded BDT 6,00,000. Below that, AIT is not triggered.

Q5. What is the penalty for filing a tax return after Tax Day? Under Section 174 of the Income Tax Act 2023: higher of 10% of the last assessed tax or BDT 1,000 per day of delay, capped at 50% of total tax payable (with a BDT 5,000 minimum). The return itself can still be filed under self-assessment.

Q6. Do I still need DVS for my audited accounts? Yes. The Document Verification System (DVS) reference, jointly maintained by NBR and ICAB, is mandatory for corporate returns. Without a valid DVS code on your audited statements, the return is incomplete and the DCT can proceed to best-judgement assessment.

Final Thoughts

The tax and VAT compliance calendar Bangladesh for FY 2025-26 is busier than ever, but it is also more navigable than at any point in the last decade — provided your finance function treats compliance as a monthly discipline, not a year-end scramble. The legal infrastructure has tightened, the digital tools have matured, and the cost of getting it wrong is sharper than the cost of getting it right.

If you take one thing from this guide, let it be this: every deadline in the calendar above has, at one point or another, ended up as a six- or seven-figure penalty for a company I have advised. Every single one of those liabilities could have been avoided by a calendar entry, an owner, and a reminder.

Bookmark this page. Print the calendar in Part 2 below. Share it with your accounts team, your auditor, and your finance leadership. Then revisit it every quarter — because Bangladesh’s tax landscape is moving quickly, and the practitioners who stay ahead of the SROs will be the ones who keep their clients and their employers out of avoidable disputes.

Have a question on a specific deadline, an NBR notice, or a transfer pricing position? Drop it in the comments — I respond to every genuine query, and corrections from fellow practitioners are always welcome. The compliance community in Bangladesh gets stronger when we keep each other accurate.

Word count: ~3,150 words | Primary keyword “tax and VAT compliance calendar Bangladesh” used 10 times

PART 2: THE CALENDAR PAGE CONTENT

SEO Meta Package

| Element | Content | Length |

|---|---|---|

| SEO Title | Tax & VAT Compliance Calendar Bangladesh FY 2025-26 | 53 chars |

| Meta Description | Complete FY 2025-26 tax and VAT compliance calendar for Bangladesh. Every NBR, RJSC, and Bangladesh Bank deadline with forms, sections, and authorities. | 153 chars |

| URL Slug | compliance-calendar-bangladesh-2025-26 | 39 chars |

PAGE BODY

Tax & VAT Compliance Calendar Bangladesh — FY 2025-26

Last updated for FY 2025-26 by Md Rakib Hassan, Income Tax Practitioner

A consolidated, printable tax and VAT compliance calendar Bangladesh finance teams can pin to the wall. Every recurring filing, with the form, the legal section, the authority, and the deadline.

🔵 MONTHLY DEADLINES

| # | Compliance | Form | Deadline | Authority | Legal Basis |

|---|---|---|---|---|---|

| 1 | Monthly VAT Return | Mushak 9.1 | 15th of next month | VAT Commissionerate / vat.gov.bd | Sec 64, VAT & SD Act 2012 |

| 2 | VAT Payment (net payable) | Treasury Challan | 15th of next month | Designated bank | Sec 64, VAT & SD Act 2012 |

| 3 | VDS Deposit | VDS Challan | 7th of next tax period | VAT Commissionerate | SRO 182/2025 |

| 4 | TDS Deposit | Treasury Challan | Within 2 weeks of deduction | Sonali Bank / AD bank | Sec 142, ITA 2023 |

| 5 | Monthly Withholding Tax Statement | Prescribed format | 25th of next month | Deputy Commissioner of Taxes (DCT) | ITA 2023 |

🟢 QUARTERLY DEADLINES

| # | Compliance | Form | Deadline | Authority | Legal Basis |

|---|---|---|---|---|---|

| 6 | AIT Q1 (25%) | Treasury Challan | 15 September 2025 | DCT | Sec 154, ITA 2023 |

| 7 | AIT Q2 (25%) | Treasury Challan | 15 December 2025 | DCT | Sec 154, ITA 2023 |

| 8 | AIT Q3 (25%) | Treasury Challan | 15 March 2026 | DCT | Sec 154, ITA 2023 |

| 9 | AIT Q4 (25%) | Treasury Challan | 15 June 2026 | DCT | Sec 154, ITA 2023 |

| 10 | Withholding Tax Return Q1 (Jul-Sep) | Sec 177 return | 31 October 2025 | DCT | Sec 177, ITA 2023 |

| 11 | Withholding Tax Return Q2 (Oct-Dec) | Sec 177 return | 31 January 2026 | DCT | Sec 177, ITA 2023 |

| 12 | Withholding Tax Return Q3 (Jan-Mar) | Sec 177 return | 30 April 2026 | DCT | Sec 177, ITA 2023 |

| 13 | Withholding Tax Return Q4 (Apr-Jun) | Sec 177 return | 31 July 2026 | DCT | Sec 177, ITA 2023 |

| 14 | FDI Quarterly Return | ED Form / Statistical Return | Within 20 days of quarter-end | Bangladesh Bank via AD bank | FE Regulations |

🟡 ANNUAL DEADLINES

Income Tax Returns

| # | Compliance | Form | Deadline | Authority |

|---|---|---|---|---|

| 15 | Corporate Tax Return — July-June year-end | IT-GHA / Sec 166 | 15 January 2026 (Tax Day) | DCT |

| 16 | Corporate Tax Return — Jan-Dec year-end | IT-GHA / Sec 166 | 15 September 2026 (Tax Day) | DCT |

| 17 | Individual Tax Return AY 2025-26 | IT-11GA | 30 November 2025 (extended to 31 Jan 2026) | DCT via etaxnbr.gov.bd |

| 18 | Employee Tax Return (Sec 180) | Salary statement | 30 November 2025 | DCT |

| 19 | Transfer Pricing Return | TP Statement | With corporate return | DCT |

| 20 | International Transaction Return | Sec 238 return | With corporate return | DCT |

Mandatory Attachments to Corporate Return

- Audited financial statements (signed by ICAB-registered CA)

- Valid DVS reference number

- Tax computation sheet (book-to-tax reconciliation)

- Statement of International Transactions (where applicable)

- Transfer Pricing report (where threshold breached)

Statutory and Regulatory Filings

| # | Compliance | Form | Deadline | Authority |

|---|---|---|---|---|

| 21 | RJSC Annual Return | Schedule X | Within 30 days of AGM | RJSC |

| 22 | AGM (subsequent) | — | Within 15 months of last AGM | Company secretary |

| 23 | Trade Licence renewal | — | By 30 June 2026 | City Corporation / Pourashava |

| 24 | IRC renewal | — | By 30 June 2026 | CCI&E |

| 25 | ERC renewal | — | By 30 June 2026 | CCI&E |

| 26 | Fire Licence renewal | — | As per certificate | Fire Service and Civil Defence |

| 27 | Environmental Clearance | — | As per ECC validity | Department of Environment |

| 28 | BIDA Registration | — | As per certificate | BIDA |

| 29 | Trade body memberships (BGMEA, MCCI, etc.) | — | By financial year-end | Respective body |

⚠️ KEY PENALTIES AT A GLANCE

| Default | Penalty |

|---|---|

| Late Mushak 9.1 | BDT 10,000 + 1% monthly interest |

| Late TDS deposit | 4% monthly interest + expense disallowance |

| Late VDS deposit | 2% monthly interest + up to 50% VAT penalty |

| Late corporate return | 10% of last assessed tax OR BDT 1,000/day (max 50% of payable, min BDT 5,000) |

| Sec 177 return default | 10% of tax not deducted + interest |

| Missing PSR | 50% additional TDS on payments to that party |

| RJSC Schedule X delay | Daily fine BDT 200+; risk of strike-off |

📌 FY 2025-26 KEY REGULATORY UPDATES

- NBR dissolved (12 May 2025). Replaced by Revenue Policy Division (RPD) and Revenue Management Division (RMD) under the Ministry of Finance via the Revenue Policy and Revenue Management Ordinance 2025.

- Mandatory e-filing for individuals from 4 August 2025 via etaxnbr.gov.bd.

- Finance Ordinance 2025 (issued 2 June 2025) — repealed Section 20 (income difference tax); raised presumptive tax from 0.6% to 1%; exempted funds from filing.

- Withholding TDS statement continues to be due on the 25th (not 15th) of the following month.

- e-VAT digitisation — hard-copy returns must be migrated through the iVAS portal by 31 March 2026.

💡 HOW TO USE THIS CALENDAR

- Print and pin this tax and VAT compliance calendar Bangladesh at the desk of every finance team member.

- Assign a single owner to each row.

- Set T-7 internal deadlines to leave room for challan and DVS issues.

- Reconcile monthly — TDS, VAT, payroll, and supplier ledgers.

- Review quarterly with your auditor or tax advisor.

Prepared and maintained by Md Rakib Hassan, Income Tax Practitioner (10+ years, Bangladesh & UK). For SROs, NBR notifications, or audit dispute support, reach out via the contact page.

Disclaimer: This calendar reflects the regulatory position as of FY 2025-26 based on the Income Tax Act 2023, Finance Ordinance 2025, the VAT and Supplementary Duty Act 2012, and notifications issued through Q1 2026. Deadlines may be extended or amended through subsequent SROs — always verify against the latest RMD/NBR notification before filing.

Leave a Reply

You must be logged in to post a comment.