Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

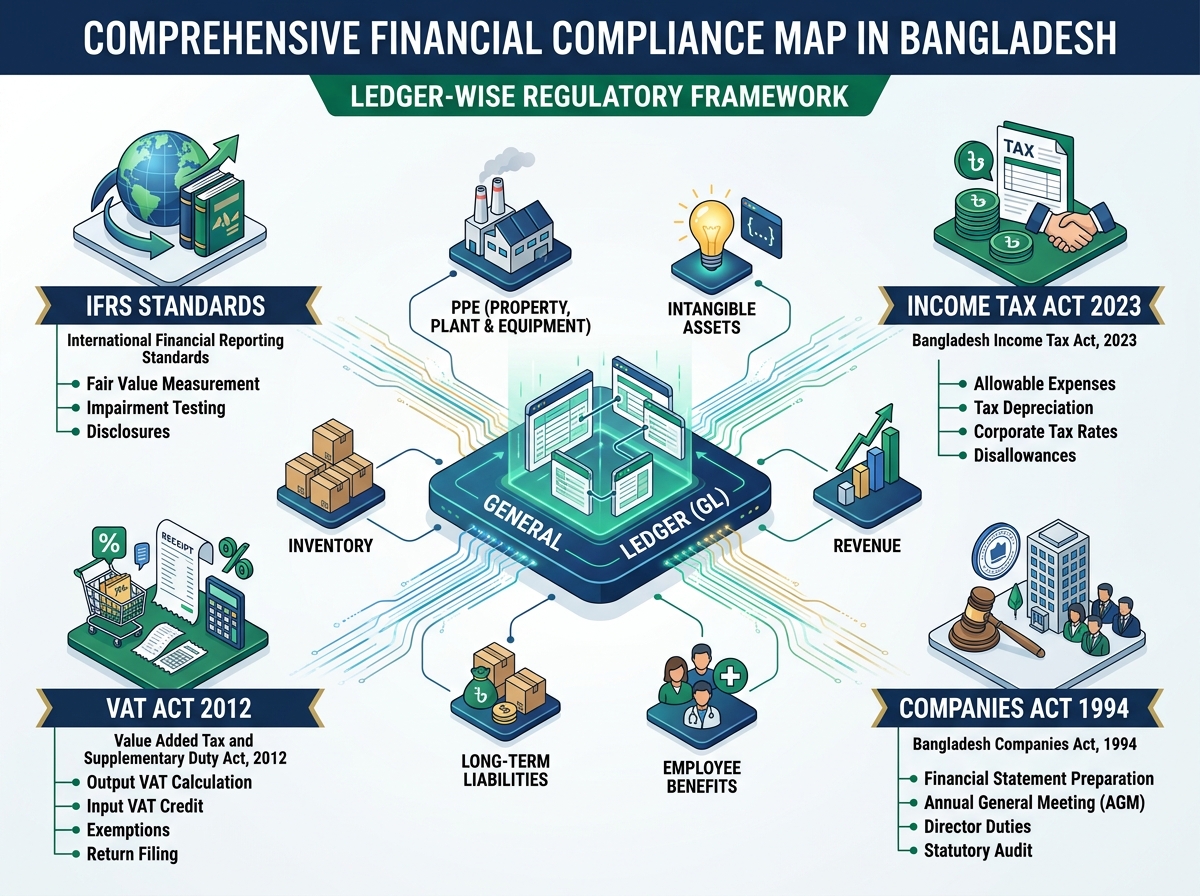

One of the most underappreciated skills in Bangladeshi finance is knowing which law applies to which ledger head — and why. Every time you close a month, prepare a tax return, or respond to an NBR or VAT audit query, you are navigating the intersection of at least four different frameworks simultaneously: IFRS/IAS standards, the Companies Act 1994, the Income Tax Act 2023, and the VAT & SD Act 2012.

Most professionals know each of these in isolation. Far fewer know how they interact — ledger by ledger — and that gap is exactly where compliance errors happen.

This guide maps the key ledger heads in a standard Bangladeshi financial statement against each of the four frameworks, giving you a practical reference for your day-to-day compliance work.

Why Ledger-Wise Mapping Matters

When the NBR sends an audit notice, they do not ask about “tax compliance in general.” They ask about specific transactions — a particular fixed asset addition, a set of receivables, a contractor payment, an interest expense. Each of those transactions sits under a specific ledger head, and each ledger head has its own compliance obligations across multiple laws.

The same fixed asset purchase, for example, involves:

- IAS 16 for recognition, measurement, and depreciation

- Companies Act Section 186 / Schedule XI for disclosure in financial statements

- Income Tax Act 2023 Schedule 6 for tax depreciation (which differs from accounting depreciation)

- VAT Act Section 15 for input VAT credit on the purchase

Get any one of these wrong and you have a compliance gap — even if everything else is perfectly correct.

This is what ledger-wise IFRS, VAT and tax compliance in Bangladesh means in practice.

Non-Current Assets

Property, Plant and Equipment (PPE)

IFRS/IAS Standard: IAS 16 — Property, Plant and Equipment

IAS 16 requires PPE to be recognised at cost and subsequently measured either at cost less accumulated depreciation (cost model) or at revalued amount (revaluation model). Useful life and residual value must be reviewed at each year-end.

Companies Act 1994: Section 186 and Schedule XI require PPE to be disclosed in the fixed assets schedule with opening balance, additions, disposals, depreciation for the year, and closing net book value.

Income Tax Act 2023: Schedule 6 of the Act provides specific depreciation rates for tax purposes — these are different from accounting depreciation rates under IAS 16. The most commonly encountered difference is that tax depreciation rates are prescribed (e.g., 10% for furniture, 20% for vehicles, 10% for general plant), while accounting depreciation is based on useful life estimates. This difference creates temporary differences that must be accounted for under IAS 12 as deferred tax.

VAT Act 2012: Section 15 allows input VAT credit on the purchase of capital goods used for taxable supplies. However, if the asset is used for both taxable and exempt supplies, input VAT credit must be claimed proportionately. The First Schedule of the VAT Act exempts certain capital equipment — particularly for specific industries — from VAT at import or purchase stage.

Practical tip: When adding a new fixed asset, check three things: (1) Is input VAT claimable on the purchase? (2) What is the tax depreciation rate under Schedule 6? (3) Does the accounting useful life differ from the tax depreciation rate — if so, create a deferred tax workings entry.

Intangible Assets

IFRS/IAS Standard: IAS 38 — Intangible Assets

Internally generated intangibles (except development costs meeting IAS 38 capitalisation criteria) cannot be capitalised. Acquired intangibles (software, patents, licences) are capitalised at cost and amortised over useful life.

Income Tax Act 2023: Section 2(46) covers the taxable entity definition; Schedule 6 provides amortisation allowances for intangibles for tax purposes. TDS under Section 91 (10% on base value) applies when making payments for intangible assets to third parties. This is a commonly missed withholding obligation — companies often pay software licence fees or royalties without applying Section 91 TDS.

VAT Act 2012: Section 15 allows input VAT on intangible services. The First Schedule may exempt certain software services.

Watch point: Royalty payments to non-residents for intangible assets attract Section 119 TDS at 20% (non-resident rate) — this is separate from Section 91 which applies to residents. Always check whether the intangible payment recipient is resident or non-resident.

Right-of-Use Assets (Leases)

IFRS/IAS Standard: IFRS 16 — Leases

IFRS 16 requires lessees to recognise a right-of-use (ROU) asset and a lease liability for most leases. The standard eliminates the operating/finance lease distinction from the lessee’s perspective (with limited exceptions for short-term and low-value leases).

Income Tax Act 2023: Lease deductions under the chapter on business income are available for the interest component of the lease liability (not the full lease payment). This is a key difference from the older treatment where the full lease rental was deductible. Finance teams must maintain a proper lease amortisation schedule to correctly identify the deductible portion.

VAT Act 2012: Section 15 allows input VAT credit on VAT paid for leased assets. Section 55 covers supplementary duty on leased services where applicable. For office space leases, VDS under service code S074.00 at 15% applies on the rent payment.

Investment Property

IFRS/IAS Standard: IAS 40 — Investment Property

Investment property is measured either at cost or at fair value. If fair value model is used, changes in fair value go to profit or loss — creating significant temporary differences for deferred tax purposes.

Income Tax Act 2023: Section 104 covers tax on property income (rental income from investment property). TDS under Section 109 at 10% applies on house rent payments — so if your company is a tenant, you must deduct 10% from your rent and deposit it as TDS.

VAT Act 2012: Section 15 covers VAT on property leasing. The First Schedule may exempt certain property types. VDS at 15% (S074.00) applies on commercial property rent payments.

Current Assets

Inventories

IFRS/IAS Standard: IAS 2 — Inventories

IAS 2 requires inventories to be measured at the lower of cost and net realisable value (NRV). FIFO or weighted average cost formulas are permitted; LIFO is prohibited under IFRS.

Income Tax Act 2023: The chapter on business income governs inventory valuation for tax purposes. Tax authorities may challenge write-downs to NRV if not adequately supported. Maintain documentation of slow-moving stock reviews and market price evidence.

VAT Act 2012: Section 15 allows input VAT credit on inventory purchases. Section 55 covers supplementary duty on manufactured goods (where applicable under the Second Schedule). The critical compliance point: if inventory is used for both taxable and exempt supplies, input VAT must be proportionately claimed — claiming full input VAT on inventories used for exempt supplies is a common audit finding.

Trade and Other Receivables

IFRS/IAS Standard: IFRS 9 — Financial Instruments

IFRS 9 requires receivables to be measured at amortised cost (for most trade receivables) with an expected credit loss (ECL) provision. The simplified approach (using a provision matrix) is permitted for trade receivables without a significant financing component.

Income Tax Act 2023: Section 104 covers TDS on interest income from receivables. Provision for bad debts is a disallowed deduction under the Income Tax Act until the debt is actually written off and proven irrecoverable. This creates a common timing difference: you provision for bad debt in your accounts (reducing profit) but cannot deduct it for tax until write-off conditions are met.

VAT Act 2012: Section 15 governs output VAT on sales. When a receivable arises from a taxable sale, the output VAT has already been charged to the VAT return. If the debt later becomes bad and is written off, a VAT adjustment (decreasing adjustment on Mushak-6.7) may be available — but only under prescribed conditions.

Advance Income Tax

IFRS/IAS Standard: IAS 12 — Income Taxes

Advance income tax (TDS/TCS paid on company income) is classified as a current asset — specifically as part of tax prepayments or advance tax. It is offset against the current tax provision.

Income Tax Act 2023: The chapter on taxable income governs advance tax payments. Under Section 163, TDS treated as minimum tax is non-refundable (see our separate minimum tax blog). Only TDS that represents an overpayment against the final assessed tax liability (for refundable heads) generates a tax refund claim.

VAT Act 2012: No direct VAT impact. Income tax and VAT are entirely separate tax obligations.

Common error: Many company financial statements classify all TDS amounts as recoverable advance tax. This is incorrect — TDS amounts covered under Section 163(2) (minimum tax) are non-refundable and should not be shown as recoverable assets unless the company has a genuine basis to expect refund.

Cash and Cash Equivalents

IFRS/IAS Standard: IAS 7 — Statement of Cash Flows; IFRS 9

Income Tax Act 2023: Section 2(46) covers the taxable entity. The Act provides for electronic tax refunds within 60 days of the refund order. Bank interest on cash balances is subject to TDS under Section 102 at 20% (for companies) deducted by the bank.

VAT Act 2012: General provisions cover VAT payable to treasury. Input VAT refunds (Section 15) are processed separately from income tax refunds. The two must never be confused or netted in the financial statements.

Equity

Share Capital and Share Premium

IFRS/IAS Standard: IAS 32 — Financial Instruments: Presentation

Share capital is classified as equity. Transaction costs of issuing shares are deducted from equity (not expensed in profit or loss).

Income Tax Act 2023: The chapter on capital gains covers share issuance at a premium. Under the Income Tax Act 2023, if a company issues shares at a price exceeding the face value without adequate justification, the premium may be treated as income. This is an area of increasing NBR scrutiny.

VAT Act 2012: Equity transactions are generally VAT-exempt. No output VAT on share issuances.

Income Statement Items

Revenue

IFRS/IAS Standard: IFRS 15 — Revenue from Contracts with Customers

Revenue is recognised when (or as) performance obligations are satisfied. The five-step IFRS 15 model applies: identify the contract, identify performance obligations, determine transaction price, allocate to obligations, recognise on satisfaction.

Companies Act 1994: Section 186 and Schedule XI Part II require turnover to be disclosed. Revenue must be presented net of VAT and supplementary duty in the profit and loss account.

Income Tax Act 2023: Section 2(46) and the chapter on taxable income treat business income as the primary income head. Revenue recognised under IFRS 15 is the starting point for taxable income — but timing differences (e.g., percentage-of-completion revenue in construction) may require adjustments.

VAT Act 2012: Section 15 governs output VAT on sales. Output VAT is shown as a deduction from gross revenue (or as a separate line) to arrive at net revenue. VAT must be charged at the point of supply — which under the VAT Act may differ slightly from the IFRS 15 revenue recognition point in some contracts.

Key point: Revenue for VAT purposes and revenue for income tax purposes can differ in timing and amount. Maintain a clear reconciliation between your VAT return (monthly Mushak 9.1 turnover), your income tax return (annual taxable turnover), and your IFRS financial statements. Unexplained differences between these three are a leading indicator of audit risk.

Administrative and Selling Expenses

IFRS/IAS Standard: IAS 1 — Presentation of Financial Statements

Income Tax Act 2023: Not all expenses recognised under IAS 1 are deductible for tax purposes. Common disallowed expenses include provisions (bad debt, warranty, legal claims before settlement), excessive entertainment, donations to non-approved organisations, and penalties. The tax computation must start from accounting profit and make adjustments for these disallowances.

VAT Act 2012: Section 15 allows input VAT credit on services and goods purchased for business purposes (to the extent used for taxable supplies). Input VAT on mixed-use expenses must be proportionately claimed. For TDS purposes, each expense category must be checked for applicable withholding obligations (Section 89, 90, 109, etc.).

Financial Charges (Interest Expense)

IFRS/IAS Standard: IFRS 9; IAS 23 — Borrowing Costs

IAS 23 requires borrowing costs directly attributable to the acquisition, construction, or production of a qualifying asset to be capitalised as part of the asset’s cost. Other borrowing costs are expensed.

Income Tax Act 2023: Section 104 requires TDS on interest payments. For loan interest paid to banks, the bank typically handles the reporting. However, for intercompany loans and private borrowings, the paying entity must deduct TDS under Section 104 at the applicable rate (generally 10% for resident, 20% for non-resident).

VAT Act 2012: Section 15 covers VAT on interest if applicable. Section 104 of the VAT Act covers supplementary duty on interest where listed in the Second Schedule.

Provision for Income Tax (Current and Deferred)

IFRS/IAS Standard: IAS 12 — Income Taxes

IAS 12 requires both current tax (based on taxable income for the year at enacted tax rates) and deferred tax (based on temporary differences between carrying amounts and tax bases). Under Bangladesh’s Income Tax Act 2023, the most common sources of deferred tax are:

- Accelerated tax depreciation vs. accounting depreciation

- Disallowed provisions (bad debt, warranty)

- Finance lease — difference between ROU asset and lease liability carrying amounts

- Minimum tax carried forward (only if recovery is probable)

The current corporate tax rate in Bangladesh for FY 2025-26: 27.5% for non-listed companies, 22.5% for listed companies (subject to banking channel conditions). These are the rates to use for current and deferred tax calculations under IAS 12.

Important: Deferred tax on minimum tax carry-forward (Section 163(8)–(9)) should only be recognised as a deferred tax asset if it is probable that future taxable profits will exceed minimum tax in subsequent years — applying normal IAS 12 recoverability criteria.

Key Takeaway

Ledger-wise IFRS, VAT and tax compliance in Bangladesh is not just an academic exercise — it is a practical necessity. Every significant balance sheet and income statement line has obligations under at least two of the four frameworks (IFRS, Companies Act, Income Tax Act, VAT Act), and many have obligations under all four simultaneously.

The most common compliance failures I see in practice come from teams who handle each framework in isolation: the accountant handles IFRS, the tax team handles income tax, and VAT is managed separately. What gets missed are the interactions — the input VAT credit on a fixed asset purchase, the TDS on a lease payment, the deferred tax on a disallowed provision, the VAT-income tax timing difference on revenue.

Building a ledger-wise compliance checklist for your organisation — mapping each major ledger head to its obligations across all four frameworks — is one of the most effective investments a finance team can make. It saves time during audits, reduces the risk of penalties, and creates a common language between the accounting, tax, and VAT functions.

Disclaimer: This blog is for general informational purposes only. It does not constitute professional accounting, tax or VAT advice. Always consult a qualified practitioner or refer to the official publications of the NBR, ICAB, and relevant regulatory bodies for specific guidance.

Leave a Reply

You must be logged in to post a comment.