Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

Ask any finance professional in Bangladesh which compliance task causes the most day-to-day confusion, and VDS will be near the top of the list. It is not because the concept is complicated — it is because the list of services is long, the rates vary, and the rules around when to deduct and when not to deduct are easy to misapply.

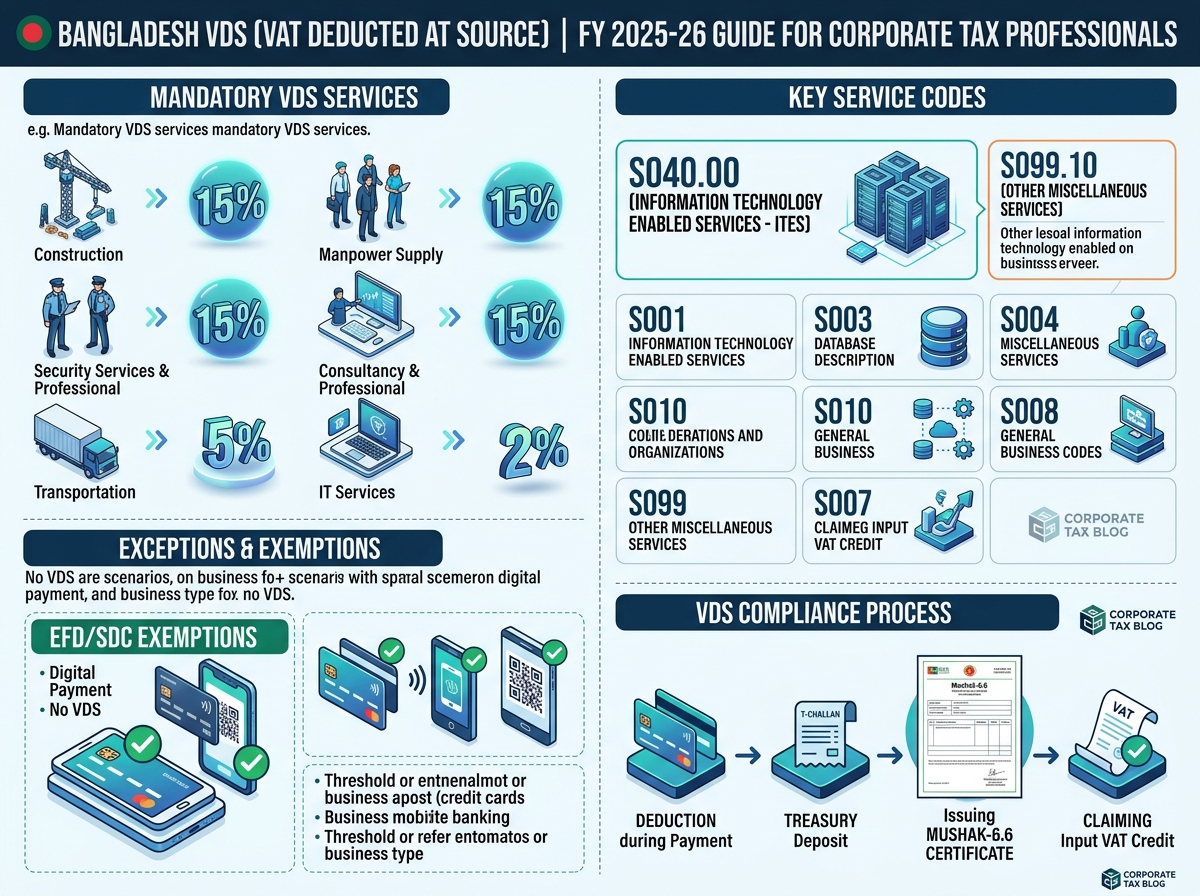

This guide gives you a complete, practical breakdown of the VDS rate in Bangladesh for FY 2025-26, covering every service code from the updated schedule, withholding entity obligations under the VDS Rules 2025 (SRO No. 182-Law/2025/310-VAT), key exceptions, and the common mistakes that get companies into trouble during VAT audits.

What Is VDS and Who Must Deduct It?

VDS stands for VAT Deducted at Source. Under Section 49 of the VAT & SD Act 2012, when a withholding entity makes a payment for certain goods or services, it must deduct VAT at the applicable rate before paying the supplier — and deposit that VAT directly to the government treasury.

VDS is triggered at the time of payment, not at invoice recording. This is a critical point. Even if you have already booked the supplier’s invoice in your accounting system, VDS applies only when you actually release the payment.

Who Is a Withholding Entity?

Under Rule 2 of the VDS Rules 2025, the following entities are legally required to deduct VDS:

- The Government, including all ministries, departments, and offices

- Any autonomous or semi-autonomous body, authority, or corporation

- Banks, insurance companies, and similar financial institutions

- NGOs approved by the NGO Affairs Bureau or the Directorate General of Social Welfare

- Educational institutions above secondary level

- Any organisation or entity with an annual turnover exceeding Tk. 10 crore

If your company’s annual turnover exceeds Tk. 10 crore, VDS compliance is mandatory for every applicable service payment you make — regardless of the size of the individual transaction.

When Is VDS NOT Required?

Before diving into the full rate table, it is equally important to know the exceptions. Under Rule 5 of the VDS Rules 2025, VDS deduction is not required in the following cases:

1. Utility services: Electricity, gas, water (WASA), telephone, internet, and similar utility bills are exempt from VDS. These are specifically excluded under Clause (Gha) of Rule 5.

2. Electronic Fiscal Device (EFD/SDC/PKI/POS) invoices: If the supplier issues a tax invoice using a government-approved electronic fiscal device, VDS is not required — the system captures the VAT electronically.

3. Certified Mushak-6.3 invoices (for specific services): For three specific services, VDS is not required if the supplier presents a VAT invoice (Mushak-6.3) certified by a Revenue Officer (RO) or Assistant Revenue Officer (ARO):

- Program content suppliers to TV and online broadcasting platforms (S043.00)

- Furniture manufacturers selling directly to end customers (S024.00) — subject to VAT at 15%

4. Procurement providers with certified VAT invoices: For procurement providers (S037.00), VDS is not required if a certified VAT invoice is produced.

Knowing these exceptions prevents unnecessary over-deduction — a compliance error that causes friction with suppliers and creates VAT reconciliation headaches.

Complete VDS Rate Chart for FY 2025-26

The following table covers all services under the VDS schedule, based on the uploaded FY 2025-26 schedule and the VDS Rules 2025. Services are marked “VAT & VDS” where both VAT and mandatory VDS apply, and “VAT” where VAT applies but VDS may not be mandatory.

Hotels, Restaurants and Catering

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 1 | S001.10 | AC Hotel | 15% | VAT & VDS |

| 1 | S001.10 | Non-AC Hotel | 10% | VAT & VDS |

| 1 | S001.20 | Restaurant | 5% | VAT & VDS |

| 2 | S002.00 | Decorators & Caterers | 15% | VAT & VDS |

Mechanical and Construction

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 3 | S003.10 | Automobile Garage & Workshop | 10% | VAT & VDS |

| 3 | S003.20 | Dockyard | 15% | VAT & VDS |

| 4 | S004.00 | Construction Firm | 10% | VAT & VDS |

| 5 | S005.10 | Go Down (Warehouse) | 15% | VAT |

| 5 | S005.20 | Port | 15% | VAT |

| 5 | S006.00 | Cold Storage | — | — |

| 13 | S013.00 | Mechanical Laundry | 15% | VAT |

| 14 | S014.00 | Indenting Organisation | 15% | VAT & VDS |

Advertising, Media and Printing

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 6 | S007.00 | Advertising Firm | 15% | VAT & VDS |

| 7 | S008.10 | Printing Press | 15% | VAT & VDS |

| 7 | S008.20 | Binding Firm | — | — |

| 39 | S039.10 | Satellite Cable Operator & Channel Distributor | 15% | VAT |

| 39 | S039.20 | Satellite Channel Distributor | 15% | VAT |

| 43 | S043.00 | Television & Online Broadcasting Media Program Supplier | 15% | VAT & VDS |

| 44 | S044.00 | BRTA Services | 15% | VAT |

| 54 | S054.00 | Advertisement in Satellite Channel Programs | 15% | VAT & VDS |

Auction, Land and Real Estate

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 8 | S009.00 | Auctioning Firm | 15% | VAT & VDS |

| 9 | S010.10 | Land Development Agency | 2% | VAT & VDS |

| 10 | S010.20 | Commercial & Residential Apartment Builders (1–1,600 sq ft) | 2% | VAT & VDS |

| 10 | S010.20 | Apartment Builders (1,601 sq ft and above) | 4.5% | VAT & VDS |

| 55 | S055.00 | Land Seller | — | VAT |

| 60 | S060.00 | Purchaser of Auctioned Goods | 15% | VAT & VDS |

Technology, Telecom and Internet

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 11 | S011.10 | Video Cassette Shop | 15% | VAT |

| 11 | S011.20 | Video Game Shop | 15% | VAT |

| 11 | S011.30 | Video, Audio Recording Shop | 15% | VAT |

| 11 | S011.40 | Video, Audio CD Rental Shop | 15% | VAT |

| 12 | S012.10 | Telephone | 15% | VAT |

| 12 | S012.11 | Tele Printer | 15% | VAT |

| 12 | S012.12 | Telex | 15% | VAT |

| 12 | S012.13 | Fax | 15% | VAT |

| 12 | S012.14 | Internet | 5% | No (EFD exemption applies) |

| 12 | S012.20 | SIM Card / e-SIM Card Supplier | 200 per SIM | No (EFD exemption) |

| 81 | S081.00 | Telecom Facility Sharing | 15% | VAT |

| 82 | S082.00 | OTT Platform | 15% | VAT |

| 83 | S099.10 | Information Technology Enabled Services | 5% | VAT & VDS |

Freight, Logistics and Transport

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 15 | S015.10 | Freight Forwards | 15% | VAT & VDS |

| 15 | S015.20 | Clearing & Forwarding Agent | 15% | VAT |

| 16 | S016.00 | Travel Agency | — | VAT |

| 35 | S035.00 | Shipping Agent | 15% | VAT |

| 36 | S036.10 | A/C Bus | 15% | VAT |

| 36 | S036.20 | A/C Launch | 15% | VAT |

| 36 | S036.30 | A/C Train | 15% | VAT |

| 48 | S048.00 | Transport Contractor (petroleum goods) | 5% | VAT & VDS |

| 48 | S048.00 | Transport Contractor (other than petroleum) | 15% | VAT & VDS |

| 49 | S049.00 | Rent-a-Car Service (excluding taxicab) | 15% | VAT |

| 77 | S077.00 | Tour Operator | 15% | No |

| 80 | S080.00 | Ride Sharing | 5% | No (EFD/app-based) |

Professional, Consulting and Financial Services

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 17 | S017.00 | Community Centre | 15% | VAT |

| 20 | S020.00 | Survey Company | 15% | VAT & VDS |

| 21 | S021.00 | Plant & Capital Machinery Rent | 15% | VAT & VDS |

| 25 | S025.00 | WASA | 15% | VAT (utility — no VDS) |

| 26 | S026.00 | Jewellery | 5% | No |

| 27 | S027.00 | Bima Company (Insurance) | 15% | VAT |

| 32 | S032.00 | Consulting & Supervisory Firm | 15% | VAT & VDS |

| 33 | S033.00 | Izaradar (Lessor) | 15% | VAT & VDS |

| 34 | S034.00 | Audit & Accounting Firm | 15% | VAT & VDS |

| 45 | S045.00 | Lawyers | 15% | VAT & VDS |

| 56 | S056.00 | Banking & Non-Banking Service Provider | 15% | VAT |

| 61 | S061.00 | Credit Card Provider Institution | 15% | VAT |

| 62 | S062.00 | Money Changer | 15% | VAT |

| 67 | S067.00 | Immigration Advisor | 15% | VAT & VDS |

| 68 | S068.00 | Coaching Centre | 15% | VAT |

| 75 | S075.00 | Stock & Security | — | VAT |

| 76 | S076.00 | Social & Sports Club | 10% | No |

| 83 | S099.50 | Credit Rating Agency | 15% | VAT & VDS |

Security, Manpower and Events

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 28 | S028.00 | Courier & Express Mail Service Provider | 15% | VAT & VDS |

| 30 | S030.00 | Beauty Parlour | 15% | VAT |

| 31 | S031.00 | Repairing & Servicing Centre | 15% | VAT & VDS |

| 37 | S037.00 | Procurement Provider | 10% | VAT & VDS |

| 38 | S038.00 | Cultural Programme with Foreign Artist | 15% | VAT |

| 40 | S040.00 | Security Service | 15% | VAT & VDS |

| 41 | S041.00 | Marriage Media | 15% | VAT |

| 46 | S046.00 | Health Club & Fitness Club | 15% | VAT |

| 47 | S047.00 | Sports Arranger | 15% | No |

| 52 | S052.00 | Sound & Light Equipment Rental | 15% | VAT & VDS |

| 53 | S053.00 | Participant in Company Board Meetings | 15% | VAT & VDS |

| 57 | S057.00 | Current Distributor | 5% | No |

| 58 | S058.00 | Chartered Aeroplane or Helicopter Rental | 15% | VAT & VDS |

| 71 | S071.00 | Programme Organizer | 15% | VAT & VDS |

| 72 | S072.00 | Manpower Supply or Management Agency | 15% | VAT & VDS |

| 73 | S073.00 | Manpower Export Agency | 15% | VAT |

Architecture, Engineering and Design

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 50 | S050.10 | Architect/Interior Designer or Decorator | 15% | VAT & VDS |

| 50 | S050.20 | Graphic Designer | 15% | VAT & VDS |

| 51 | S051.00 | Engineering Firms | 15% | VAT & VDS |

| 59 | S059.00 | Glass Sheet Laminating Organisation | 15% | VAT |

Furniture, Retail and Miscellaneous

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 24 | S024.10 | Furniture Manufacturer (selling directly) | 7.5% | VAT & VDS |

| 24 | S024.20 | Furniture Sales Centre (with prior-stage VAT challan) | 7.5% | VAT & VDS |

| 22 | S022.00 | Sweetmeat | 15% | No |

| 23 | S023.10 | Cinema Hall | 10% | No |

| 23 | S023.20 | Cinema Distributor | 10% | No |

| 18 | S018.00 | Cinema Studio | 15% | VAT |

| 19 | S019.00 | Photo Maker | — | — |

| 29 | S029.00 | Astrologer | 15% | VAT |

| 42 | S042.00 | Auto or Mechanical Saw Mill | 15% | No |

| 63 | S063.00 | Tailoring Shop (AC) | 15% | No |

| 64 | S064.10 | Amusement Park & Theme Park | 15% | VAT |

| 64 | S064.20 | Touristic Floors & Structures (Historical Places) | 15% | VAT |

| 65 | S065.00 | House Cleaning & Maintenance Organisation | 15% | VAT & VDS |

| 66 | S066.00 | Lottery Ticket Seller | 15% | VAT & VDS |

| 69 | S069.00 | English Medium School | 5% | No |

| 70 | S070.10 | Private University | 15% | VAT |

| 70 | S070.20 | Private Medical & Engineering College | 15% | VAT |

House Rent, Office Rent and Branded Showroom

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 74 | S074.00 | House Rent / Office Rent | 15% | VAT & VDS |

| 78 | S078.00 | Branded RMG Showroom | 7.5% | No |

Other Miscellaneous Services

| SL | Service Code | Service Name | VAT Rate | VDS |

|---|---|---|---|---|

| 84 | S099.20 | Other Miscellaneous Services | 15% | VAT & VDS |

| 85 | S099.30 | Sponsorship Services | 15% | VAT |

| 86 | S099.40 | Meditation | 5% | No |

| 87 | S099.60 | Online Goods Selling | 15% | No |

A Practical Worked Example: Two Services in One Payment Run

Your company’s accounts payable team is processing payments this week for:

Payment 1 — Security firm bill: Tk. 3,00,000 Service code: S040.00 | VDS rate: 15% VDS to deduct: Tk. 45,000 Net payment to supplier: Tk. 2,55,000

Payment 2 — Freight forwarding agent bill: Tk. 1,50,000 Service code: S015.10 | VDS rate: 15% VDS to deduct: Tk. 22,500 Net payment to supplier: Tk. 1,27,500

Payment 3 — Internet service bill: Tk. 50,000 Service code: S012.14 | VDS rate: 5% — but EFD exemption applies if the ISP issues through EFD/SDC No VDS required if EFD invoice is provided

Both VDS amounts (Tk. 45,000 + Tk. 22,500 = Tk. 67,500) must be deposited to the government treasury using economic code 1141101 by the 15th of the following month.

The supplier must be issued a Mushak-6.6 (VDS certificate) acknowledging the VAT deducted. Without this certificate, the supplier cannot claim the deducted VAT as their input tax credit.

The New VDS Rules 2025: What Changed?

The VDS Rules 2025 (SRO No. 182-Law/2025/310-VAT) replaced the earlier VDS Rules 2021 (SRO No. 240-Law/2021/163-VAT) effective from FY 2025-26. Key changes include:

The mandatory VDS list expanded from 43 to 44 services. Programme organiser (S071.00) is now added as a mandatory VDS service.

Withholding entity threshold for annual turnover remains at Tk. 10 crore. No change here, but enforcement is tightening. NBR is increasingly cross-matching VDS deposit records against company VAT returns.

EFD/SDC exemption is now more explicitly codified. If a supplier’s invoice is generated through an approved electronic fiscal device, VDS is not required — the electronic system captures the transaction directly. This applies to internet services, certain retail payments, and ride-sharing services.

Historical SRO reference list updated. The uploaded document references the full chain of VDS SROs from FY 2015-16 through to FY 2025-26 (SRO No. 160-Law/2024/268-VAT, dated 27 June 2024, as amended in 2025).

Common VDS Mistakes That Cause Audit Problems

1. Not issuing Mushak-6.6 to the supplier after deduction. The VDS certificate is not optional. Without it, the supplier cannot claim their deducted VAT. Non-issuance is a compliance failure on your part.

2. Deducting VDS on utility bills. Electricity, gas, WASA, telephone, and internet (where EFD applies) are exempt. Many companies still deduct VDS on these — and then face disputes with utility providers.

3. Using the wrong VAT rate for the service. Security services (S040.00) are 15%, but transport contractor for petroleum (S048.00) is only 5%. These mix-ups cause mismatches between your VDS deposit and the supplier’s VAT return.

4. Missing the monthly deposit deadline. VDS collected must be deposited by the 15th of the following month. Late deposits attract interest and penalty under the VAT & SD Act 2012.

5. Failing to cross-check with supplier registration. If your supplier is not VAT-registered, different rules may apply. Always verify your supplier’s VAT registration (BIN) before processing payments.

Key Takeaway

The VDS rate in Bangladesh for FY 2025-26 is governed by the VDS Rules 2025 (SRO No. 182-Law/2025/310-VAT), covering 44 mandatory services and a range of other services with prescribed VAT rates. Most services carry a standard 15% VAT rate, with notable exceptions including restaurants (5%), IT-enabled services (5%), internet (5%), construction (10%), land development (2–4.5%), and transport of petroleum goods (5%).

For any withholding entity with annual turnover above Tk. 10 crore, VDS compliance is not optional — it is a core monthly obligation. Track your payment runs, apply the correct service code rate, issue Mushak-6.6 certificates to all suppliers, and deposit by the 15th of the following month. These four habits cover the vast majority of VDS compliance risk.

Disclaimer: This blog is for general informational purposes only. It does not constitute professional tax or VAT advice. Always consult a qualified tax practitioner or refer to the official NBR publications for specific guidance.

Leave a Reply

You must be logged in to post a comment.