Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

One question I get asked surprisingly often — especially from companies facing their first NBR audit — is: “How long do we need to keep our records?” The honest answer is: longer than most people think, and it depends on which law you are asking about.

In Bangladesh, the document retention period is governed by at least three separate laws, and each sets a different minimum period. Failing to keep records for the required duration can result in penalties, adverse assumptions during an audit, and difficulty defending your tax or VAT position.

This guide gives you a clear, practical answer to the document retention period in Bangladesh under the Income Tax Act 2023, the VAT & SD Act 2012, and the Companies Act 1994.

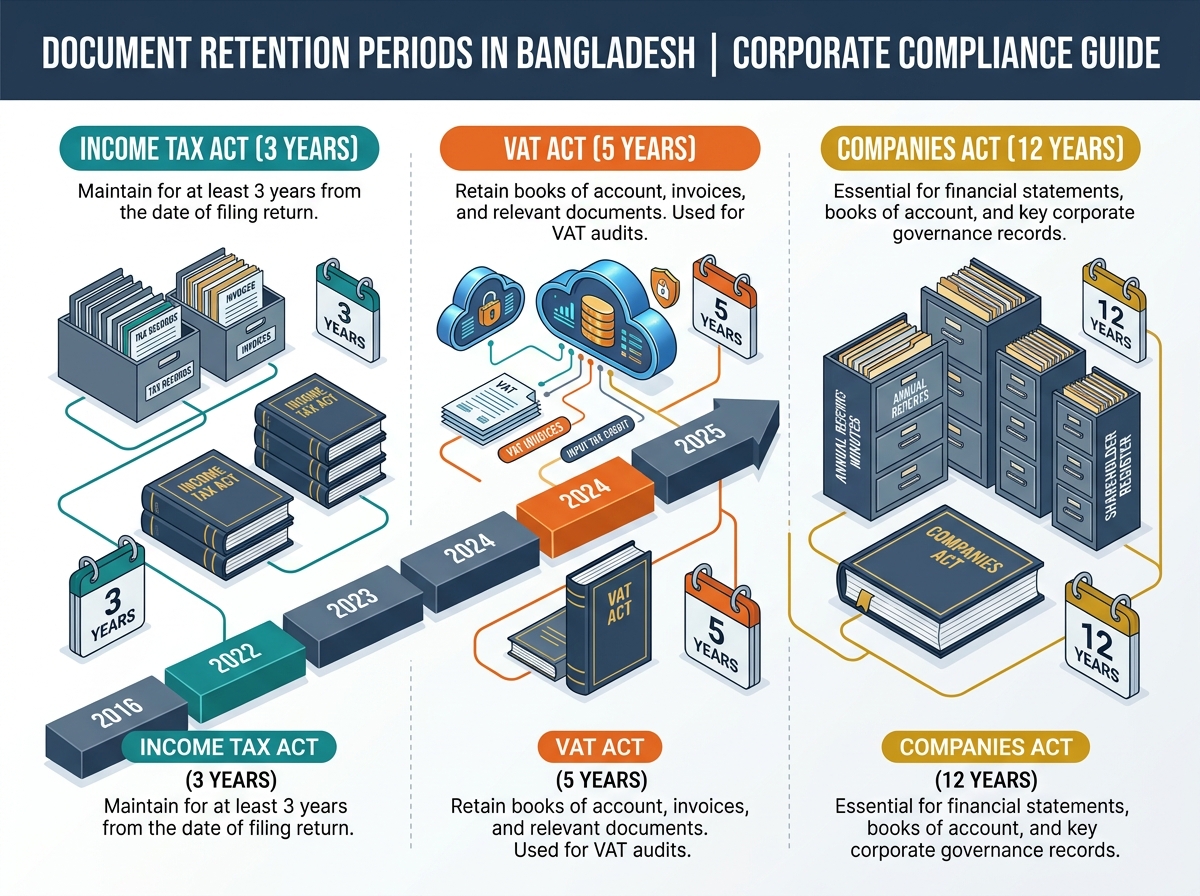

The Three Laws That Govern Document Retention in Bangladesh

| Law | Relevant Section | Minimum Retention Period |

|---|---|---|

| Income Tax Act, 2023 | Section 179 | 3 Years |

| VAT & SD Act, 2012 | Section 107 | 5 Years |

| Companies Act, 1994 | Section 181 | 12 Years |

These three periods coexist — meaning if your company is subject to all three laws (which most registered companies are), you must retain records for the longest applicable period, which is 12 years under the Companies Act.

Let us look at each in detail.

1. Income Tax: 3-Year Retention Period (Section 179, Income Tax Act 2023)

Section 179 of the Income Tax Act 2023 deals with the presentation of accounts, documents, and records to tax authorities.

Under this section, the Deputy Commissioner of Taxes (DCT) can, through written notice, ask any taxpayer to produce records related to an income year up to 3 years prior to that income year. These records may be needed for:

- A return audit

- A tax assessment

- Determination of tax liability

The types of records covered include: books of accounts, ledgers, financial statements, documents, data, and electronic records.

What does “3 years” mean in practice?

Suppose the current income year is 2024-25 (July 2024 – June 2025). The DCT can request records going back to income year 2021-22. So at any point in time, you need to have the last 3 income years’ records readily available.

Electronic records are included. Under Section 179(4)(b) and (c), “data” includes electronic data as defined under the Information and Communication Technology Act 2006, and electronic records are explicitly covered. This means your accounting software exports, email communications relevant to transactions, and digital invoices must also be retained.

Can the period extend beyond 3 years?

Yes — if there is an ongoing assessment, audit, or proceeding related to a particular income year, you must retain the relevant documents until that matter is fully resolved, even if it goes beyond 3 years. Section 179 sets the minimum, not the absolute outer limit when disputes are pending.

2. VAT: 5-Year Retention Period (Section 107, VAT & SD Act 2012)

Section 107 of the VAT & SD Act 2012 requires every registered person (i.e., every VAT-registered business) to maintain and preserve their records for 5 years from the date of the relevant transaction.

The records that must be kept under Section 107 include:

- Purchase and sales records for taxable or VAT-exempt goods, services, and immovable property, along with all related documents

- Details of goods, services, or immovable property sold, including VAT invoices and credit/debit notes

- Tax invoices issued and received, and source VAT deduction certificates

- Customs documents related to imports or exports

- Records of input-output coefficients for manufactured goods

- Records of supplementary duty applicable to services

- Treasury challans for VAT payments

- Monthly VAT return documents

- Any other prescribed records

Digital storage is allowed. Under Section 107(2A), a VAT-registered person may store records in an Enterprise Resource Planning (ERP) system or NBR-approved VAT software on a secure server. This gives companies the option to maintain digital archives rather than paper-only records — but the records must remain accessible and intact.

Important: If any VAT proceeding, assessment, or case is pending at the end of the 5-year period, records related to that matter must be kept until the case is resolved — even if it takes longer.

5 years is the most operationally demanding of the three obligations for most businesses, because the volume and variety of documents required under VAT is extensive — monthly Mushak returns, purchase and sales registers, tax invoices, customs documents, and more.

3. Companies Act: 12-Year Retention Period (Section 181, Companies Act 1994)

Section 181(5) of the Companies Act 1994 sets the most demanding standard: every company must preserve its books of account and relevant vouchers for a minimum of 12 years immediately preceding the current year.

This covers:

- All money received and spent by the company, including the sources and uses of those funds

- All purchases and sales of goods

- All assets and liabilities

- For companies engaged in manufacturing, processing, mining, or milling — records of raw materials, labour, and overhead costs

What if the company is less than 12 years old?

If the company was incorporated less than 12 years before the current year, it must preserve records for the entire period since incorporation up to the current year. No exception for young companies — all records from day one must be kept.

Consequences of non-compliance:

Under Section 181(6) and (7), any of the following persons can be held liable if required records are not maintained:

- The Managing Agent, Managing Director, or CEO

- The General Manager or Manager

- Any other officer of the company

The penalty is up to 6 months of imprisonment and/or a fine of up to Tk. 5,000 for each offence. Additionally, under Section 182(8), failure to produce records for an authorised inspection can result in up to 1 year of imprisonment and a fine of up to Tk. 10,000.

Beyond the legal penalties, the practical consequence during an audit is severe: if you cannot produce records, the assessing officer is entitled to make assumptions — almost always unfavourable to the taxpayer.

How the Three Periods Interact: A Practical Framework

Most accountants and finance managers ask: “Do we need three separate filing systems?” Not necessarily — but you do need a structured approach.

Here is a practical framework:

Years 1–3: All records must be readily accessible. These are within the income tax audit window. Keep them in active or near-active storage — whether physical files or digital folders — where they can be produced quickly in response to an NBR notice.

Years 1–5: All VAT records must also be accessible. If your company is VAT-registered (which most companies of reasonable size are), your 5-year VAT documentation obligation overlaps with, and extends beyond, the income tax window.

Years 1–12: All company-level books of account and vouchers must be preserved in good order under the Companies Act. These do not need to be in active storage, but they must be retrievable. Archived physical files in good condition, or secure digital storage, both satisfy this requirement.

Practical recommendation: Maintain a document retention policy within your finance department that categorises records by retention period. Mark each file or digital folder with its creation year and scheduled destruction date — and make sure no document is destroyed before the 12-year period under the Companies Act has passed, unless you are certain the Companies Act obligation does not apply.

What Types of Documents Are We Talking About?

Here is a practical list of documents and their applicable retention obligations:

| Document Type | Income Tax (3 yr) | VAT (5 yr) | Companies Act (12 yr) |

|---|---|---|---|

| Financial statements (P&L, Balance Sheet) | ✓ | ✓ | ✓ |

| Sales invoices | ✓ | ✓ | ✓ |

| Purchase invoices / bills | ✓ | ✓ | ✓ |

| Tax invoices (Mushak) | ✓ | ✓ | ✓ |

| Treasury challans (TDS/VAT deposits) | ✓ | ✓ | ✓ |

| Bank statements | ✓ | ✓ | ✓ |

| Customs documents (import/export) | ✓ | ✓ | ✓ |

| TDS certificates (issued/received) | ✓ | ✓ | ✓ |

| Payroll records | ✓ | — | ✓ |

| Fixed asset register | ✓ | ✓ | ✓ |

| Board minutes and resolutions | — | — | ✓ |

| Shareholder registers | — | — | ✓ |

| Loan agreements | ✓ | ✓ | ✓ |

| VAT monthly returns (Mushak 9.1) | — | ✓ | — |

Lessons From Tax Audit Experience

In audit situations I have encountered — both at the NBR and HMRC level — the most common document retention failure in Bangladesh is not outright destruction of records. It is disorganisation: documents exist but cannot be found promptly when an audit notice arrives.

An NBR audit notice typically gives you a very short window to respond. If your VAT invoices from 3 years ago are in unmarked boxes in a warehouse, or your TDS challans are scattered across multiple email accounts, you will struggle to respond on time — even if every document technically exists somewhere.

A good document retention system has three elements:

- Classification — documents sorted by type, entity, and financial year

- Indexing — a simple log or spreadsheet telling you where each type of record is stored

- Accessibility — the ability to retrieve specific documents quickly, whether digital or physical

Companies that have adopted ERP systems with built-in document management (which is now permitted under Section 107(2A) of the VAT Act) have a significant advantage in audit situations.

Key Takeaway

The document retention period in Bangladesh varies by law: 3 years under the Income Tax Act 2023 (Section 179), 5 years under the VAT & SD Act 2012 (Section 107), and 12 years under the Companies Act 1994 (Section 181). For companies subject to all three — which is the norm for most incorporated businesses — the effective minimum is 12 years.

This is not just a legal formality. In a tax environment where NBR audits, VAT assessments, and company inspections are increasing in frequency and sophistication, your document retention practice is your first line of defence. Build the system now, not after you receive the audit notice.

Disclaimer: This blog is for general informational purposes only. It does not constitute professional tax advice. Always consult a qualified tax practitioner or refer to the official publications of the NBR, VAT authority, and RJSC for specific guidance.

Leave a Reply

You must be logged in to post a comment.