Written by Md Rakib Hassan — Income Tax Practitioner with 10+ years of tax compliance and audit experience across Bangladesh and the UK. Former accounts manager at a UK chartered accounting firm managing 1,000+ clients, with direct experience resolving multi-year tax audit disputes with HMRC and the NBR. Currently Finance Controller at a UK-based multinational tech group.

Minimum tax is one of the most misunderstood concepts in Bangladesh’s income tax system. I regularly see finance teams calculate their regular tax liability, breathe a sigh of relief when the number seems reasonable — and then completely overlook the minimum tax calculation that overrides it.

If you have TDS deducted from your company’s income or if your company has gross receipts above certain thresholds, minimum tax in Bangladesh almost certainly applies to you. This guide explains how it works under Section 163 of the Income Tax Act 2023, updated for the Finance Ordinance 2025.

What Is Minimum Tax in Bangladesh?

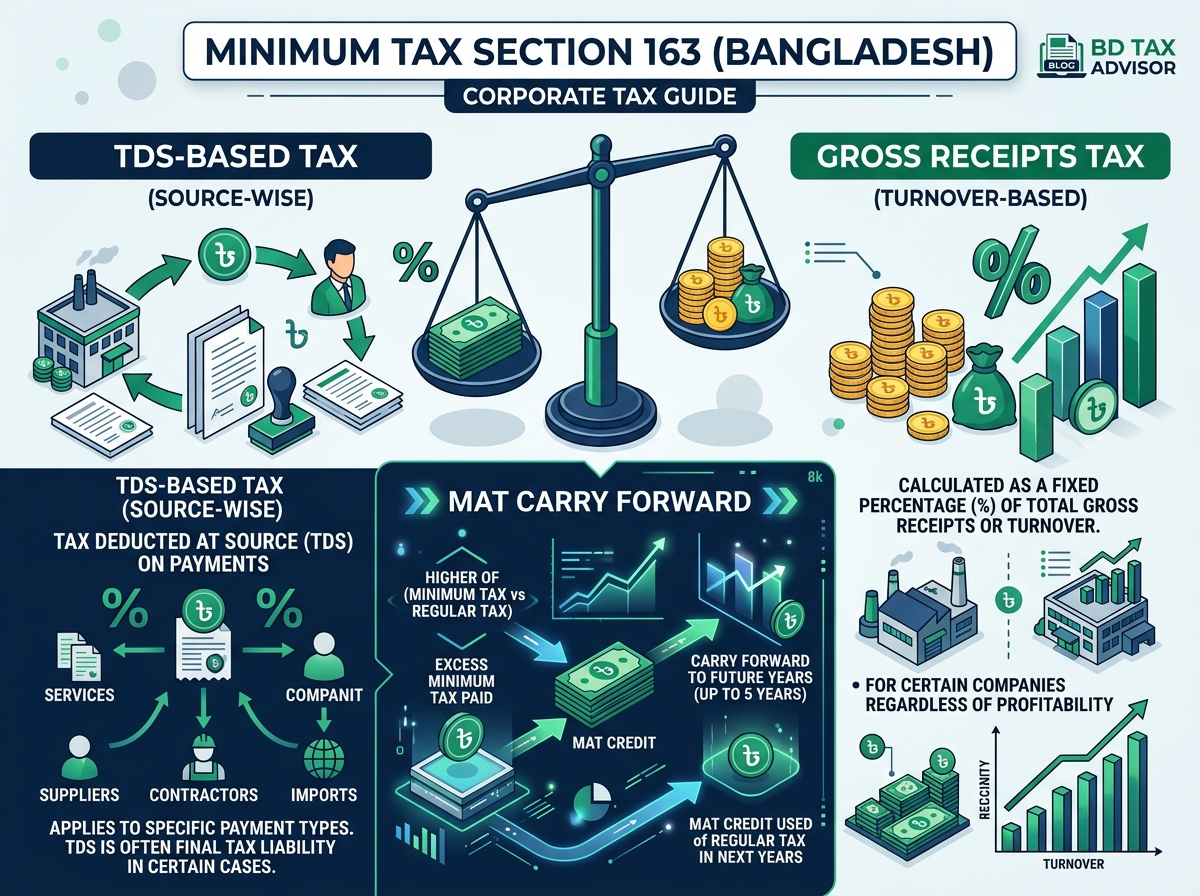

Minimum tax is a concept that ensures every business and individual pays a floor level of tax, regardless of their reported profit or loss. In Bangladesh, it works in two distinct ways under Section 163:

1. TDS-Based Minimum Tax (Section 163(2)): Certain types of TDS deducted at source are treated as minimum tax. This means even if your regular tax liability is lower than the TDS already deducted, you still pay the TDS amount — you cannot get a refund of the difference.

2. Gross Receipts-Based Minimum Tax (Section 163(5)): Companies, trusts, firms, and large individuals with gross receipts above certain thresholds must pay a minimum tax calculated as a percentage of their total gross receipts — regardless of profit or loss.

The Finance Ordinance 2025 (effective 1 July 2025) made important changes to Section 163, including replacing the previous version entirely under Ordinance No. 28 of 2025. This guide reflects those changes.

Section 163(2): TDS as Minimum Tax

Under Section 163(2), the TDS or TCS (Tax Collected at Source) deducted under 38 specific sections of the Income Tax Act 2023 is treated as minimum tax on income from those sources.

Those sections cover income from:

- Supply of goods and contracts (Section 89)

- Services (Section 90)

- Intangible assets (Section 91)

- Advertisement (Section 92)

- Commission, discount, fee (Section 94)

- Interest on savings/fixed deposits (Section 102)

- Profit on sanchaypatra (Section 105)

- Dividends (Section 117)

- Import (Section 120)

- Export proceeds (Section 123)

- Transfer of property (Section 125)

- Commercially operated motor vehicles (Section 138)

- And many others

What this means in practice: If your company sells goods and the buyer deducts TDS of Tk. 5,00,000 under Section 89, and your regular tax liability on that business works out to only Tk. 3,50,000 — you still pay Tk. 5,00,000. The TDS is the minimum. You cannot claim a refund of the Tk. 1,50,000 difference under Section 163(7)(a).

Important Exception: For industrial undertakings engaged in the production of cement, iron, iron products, ferro-alloy products, carbonated beverages, powdered milk, aluminium products, ceramic products, and insecticides — the tax collected under Section 120 (import) on goods used as their own raw materials is not treated as minimum tax. For all other industries, it is.

How to Calculate Minimum Tax Under Section 163(2): Step-by-Step

The process follows three steps:

Step 1: Identify the income from sources covered under Section 163(2). Maintain separate books of accounts for these sources as required by Section 72.

Step 2: Calculate regular tax on that income in the normal manner and apply the regular tax rate.

Step 3: Compare regular tax with the TDS/TCS already paid on those sources. Whichever is higher is the tax payable for that source.

Worked Example: Company with Import Business

ABC Ltd. is a commercial importer. During FY 2024-25:

- Revenue: Tk. 1,00,00,000

- TDS paid at import stage (Section 120 @ 5%): Tk. 5,00,000

- Profit before tax: Tk. 14,00,000

Regular tax @ 25% = Tk. 3,50,000 Minimum tax (TDS) = Tk. 5,00,000

Tax payable = Tk. 5,00,000 (whichever is higher)

The company cannot get back the Tk. 1,50,000 excess TDS over regular tax — it is the minimum tax floor.

What If You Have Both Regular and Minimum Tax Sources?

Many businesses have income from both types of sources — some covered by Section 163(2) minimum tax provisions, and some regular sources where normal tax rules apply.

In this case, Section 163(4) says:

- Calculate minimum tax separately for sources under Section 163(2)

- Calculate regular tax separately for regular sources

- The total tax payable = minimum tax for 163(2) sources + regular tax for regular sources

Crucially, a loss from one type of source cannot be set off against income from the other (Section 163(3)(c)). This is a common trap — many finance teams try to offset a loss from a regular source against income from an import or supply business, which is not permitted.

Expense Allocation Where Sources are Mixed

If your business has both regular and Section 163(2) sources, expenses must be allocated between them in proportion to gross receipts (as directed by NBR Paripatra 2023). You cannot arbitrarily assign more expenses to the minimum tax source to reduce its profit.

Section 163(5): Minimum Tax on Gross Receipts

This is sometimes called the Revenue Tax or Alternative Minimum Tax (AMT). It applies regardless of profit or loss.

Who must pay it?

- Any company, trust, firm, or association of persons with gross receipts exceeding Tk. 50 lakh

- Any individual with gross receipts exceeding Tk. 4 crore

Rates for FY 2025-26:

| Type of Taxpayer | Rate on Gross Receipts |

|---|---|

| Cigarette, bidi, chewing tobacco, smokeless tobacco, gul manufacturers | 3% |

| Carbonated beverage / sweetened beverage manufacturers | 3% |

| Mobile phone operators | 2% |

| Any individual (other than tobacco manufacturers) | 0.25% |

| All other cases | 1% |

| New industrial undertaking (first 3 years of commercial production) | 0.10% |

What counts as “gross receipts”?

- All proceeds from sale of goods (excluding VAT and supplementary duty)

- All fees or charges for services (including commission and discounts)

- All receipts from any head of income

Worked Example: Jute Exporter in a Loss Year

XYZ Jute Ltd. (non-listed company) makes a loss of Tk. 5,00,000 in FY 2024-25. Revenue = Tk. 1,00,00,000. TDS on export proceeds (Section 123 @ 1%) = Tk. 1,00,000. The company enjoys a reduced 10% tax rate under an NBR SRO.

Since the company has a loss, it must pay minimum tax under Section 163(5):

- Gross receipts-based minimum tax @ 1% = Tk. 1,00,000

- But the reduced tax rate (10%) applies proportionately: Tk. 1,00,000 × (10%/25%) = Tk. 40,000

In addition, the company has bank interest income of Tk. 2,50,000 (gross), which is a regular tax source. Regular minimum tax (1%) on this = Tk. 2,500.

Total minimum tax = Tk. 40,000 + Tk. 2,500 = Tk. 42,500

However, the TDS already paid on exports (Tk. 1,00,000) under Section 163(2) is higher than Tk. 42,500, so the company pays Tk. 1,00,000 as the effective minimum tax (whichever is higher under Section 163(6)).

Section 163(6): The “Higher of” Rule

When both Section 163(4) and Section 163(5) apply, the taxpayer pays whichever is higher:

- Minimum tax under Section 163(4) (TDS-based comparison), or

- Minimum tax under Section 163(5) (gross receipts-based)

This prevents businesses from using one calculation to escape the other.

Minimum Alternative Tax (MAT): Carrying Forward Excess Minimum Tax

One of the most taxpayer-friendly provisions in Section 163 is the ability to carry forward excess minimum tax under sub-sections (8) and (9).

If, in a given year, the minimum tax paid exceeds the regular tax, that excess can be adjusted in a future year where regular tax exceeds minimum tax.

Worked Example: MAT Carry Forward

FMC Ltd., FY 2024-25:

- Regular tax: Tk. 2,50,000

- Gross receipts minimum tax (Section 163(5)): Tk. 6,00,000

- Tax payable: Tk. 6,00,000

- Excess minimum tax over regular tax = Tk. 3,50,000 → carried forward

FMC Ltd., FY 2025-26:

- Regular tax: Tk. 7,50,000

- Gross receipts minimum tax: Tk. 6,50,000

- Tax payable: Tk. 7,50,000 (regular tax is higher)

- Regular tax exceeds minimum tax by Tk. 1,00,000 → adjust Tk. 1,00,000 from the Tk. 3,50,000 carried forward

- Remaining Tk. 2,50,000 carried forward to the next year

This carry-forward mechanism makes minimum tax significantly less painful over time for businesses with cyclical profitability.

Final Tax Under Section 163(11)

Section 163(11) treats TDS from certain sources as the final discharge of tax liability — meaning no further tax, no further return obligation for that specific income. These are:

- Income heads under Section 30 — for persons exempted from filing returns under Section 166(2)

- Profit on sanchaypatra (Section 105) — for any natural person (individual)

- Compensation for acquisition of property (Section 111) — for any natural person

- Export cash subsidy (Section 112) — for any taxpayer

- Transfer of property (Section 125) — for any natural person

For example, if Mr. Ahmed receives sanchaypatra profit and TDS of Tk. 50,000 was deducted, that Tk. 50,000 is his final tax — he does not need to calculate or pay anything more for that income.

What Has Changed Under Finance Ordinance 2025?

The Finance Ordinance 2025 made several notable changes to minimum tax provisions:

- Section 163 was substituted entirely by Ordinance No. 28 of 2025 (effective 1 July 2025), consolidating and clarifying earlier provisions

- Mobile phone operator minimum tax rate changed from 1.5% to 2% of gross receipts

- Individual threshold for gross receipts minimum tax increased to Tk. 4 crore (from Tk. 3 crore)

- Carry-forward mechanism in sub-sections (8) and (9) was formally codified and clarified, with a correction in the cross-reference numbering

- A new sub-section (12) was added — any surcharge, additional interest, or additional amount payable under the Act is payable on top of minimum tax and final tax

Key Mistakes to Avoid

- Not maintaining separate books for minimum tax and regular tax sources. Section 163(3)(a) requires it. Without separate books, NBR can disallow your expense allocations.

- Trying to offset losses between different source types. You cannot. Section 163(3)(c) is explicit.

- Claiming a refund of excess TDS over regular tax. Under Section 163(7)(a), minimum tax (Section 163(2)) is non-refundable.

- Ignoring the gross receipts minimum tax for loss-making years. Even if your company made a loss, the gross receipts minimum tax (Section 163(5)) still applies.

- Not tracking the carry-forward balance. The MAT carry-forward under Section 163(8)–(9) can be a meaningful asset — keep a record of it in your tax workings.

Key Takeaway

Minimum tax in Bangladesh under Section 163 of the Income Tax Act 2023 operates on two tracks simultaneously — TDS-based (where the higher of TDS paid or regular tax is due) and gross receipts-based (where a percentage of turnover is payable regardless of profit). Finance Ordinance 2025 has updated and clarified this framework effective 1 July 2025.

For any finance professional managing company tax compliance in Bangladesh, Section 163 must be computed every year — not just in loss years, and not just when TDS is high. It is a permanent fixture of the tax calculation, and understanding it correctly is what separates accurate tax filing from costly errors.

Disclaimer: This blog is for general informational purposes only. It does not constitute professional tax advice. Always consult a qualified tax practitioner or refer to the official NBR publications for specific guidance.

Leave a Reply

You must be logged in to post a comment.